The Everything Bubble: Markets At A Crossroads

After Jerome Powell’s Brookings Institution speech, markets are caught in the middle. Participants are trying to sniff out the first signs of a pivot. Is the bottom in or is more pain on the horizon?

Relevant Past Articles:

Powell’s Speech And Contracting ISM PMI

Today, we want to zoom out and revisit the broader macroeconomic picture and analyze some of the latest data that came out this week, which will heavily influence the market direction over the next few months.

After Jerome Powell’s Brooking Institution speech yesterday, it’s clear that markets are chomping at the bit to move higher with any possible Federal Reserve narrative and pivot scenario. There’s over-hedging, short squeezes, options market dynamics and forced buying. This is beyond our expertise to say exactly why markets are exploding with volatility on any given data point or new Powell speech. However, these types of events and market movements have nearly always been a sign of unhealthy and heightened volatile swings in bear markets. Despite more talk from Powell with nothing new really said, markets perceived the speech as more “dovish” with his commentary around the concern of overdoing rate hikes. Yet, if this is another bear market rally taking shape for the major indices, we seem to be close to that rally turning over yet again.

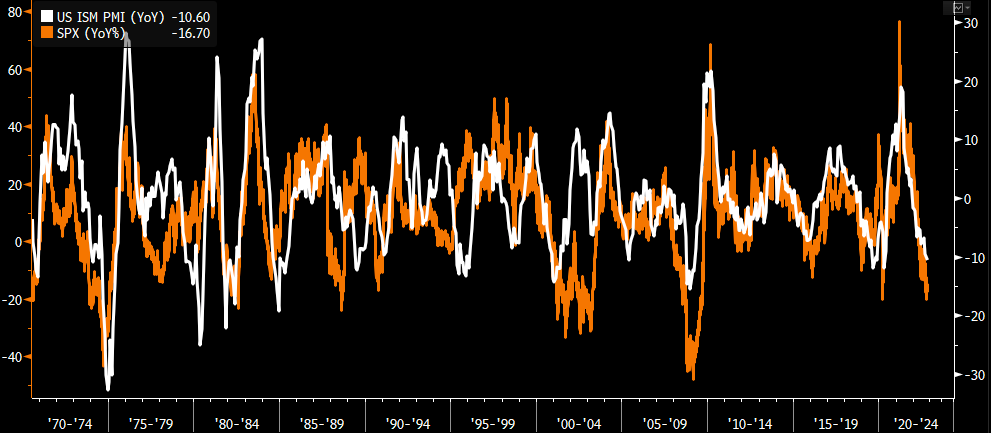

What is also concerning and expected to continue, is the trend of economic contraction as told by the data from the ISM manufacturing index (PMI). Today’s latest release shows a print of 49.0 below market expectations of 49.7. New orders are contracting, the backlog of orders are contracting and prices are decreasing. By all measures and survey responses, these are the signs of demand softening, conditions worsening and the economy moving into more cautious territory. The ISM PMI data highly correlates to the less impactful Chicago PMI data which just printed contraction lows similar to 2000, 2008 and 2020. This is the sign of an economic recession starting in the manufacturing sector.

Source: GMI, Julien Bittel

In case you missed it: Bitcoin Magazine PRO hosted American Hodl for a discussion on the bear market, the future of bitcoin and how he thinks about market strategy in one of the world’s most volatile assets.

What does economic contraction mean for financial markets? It’s typically bad news when there’s a sustained contraction trend of ISM PMI below 50 and even below 40 playing out. Shown below is the highly correlated trend of S&P 500 annual performance compared to the ISM PMI data. Typically, markets will lead the contraction reversal, but it seems we’re in the early stages of a larger contraction trend playing out: The despair phase of the market.

Source: Bloomberg, Kevin Kelly

The specific question for the bitcoin and macro relationship is now: Was this industry-leverage wipeout and capitulation event enough selling to mute the potential probability and effects of an equity bear market meltdown? Will bitcoin flatline and form a bottom if equities are to follow similar past bear market drawdown paths?

Interview appearance: Bitcoin Magazine PRO Head of Market Research Dylan LeClair appeared at Going Digital to talk with hosts Daniela Cambone and Darcy Daubaras to discuss his Bitcoin thesis and why he sees bitcoin as a “superior engineering solution” to gold.

The S&P 500 index reached a peak drawdown from all-time high of 24.82% so far and is currently 14.25% down from all-time highs during the popping of the great everything bubble in a once-in-a-century macroeconomic environment. Either we’re already out of the woods and into a new paradigm of capped downside or we’ve yet to enter the real painful period of this cyclical unwind.

We’ve still yet to see a real blowout in stock market volatility which has always impacted bitcoin. It’s been a core part of our thesis this year that bitcoin will follow traditional equity markets to the downside.

The Federal Reserve’s preferred measure of inflation also came out today, showing the second-lowest monthly rise in core personal consumption expenditures (PCE) this year at 0.2%. The annual inflation rate is still at 5% which is what the Fed says they want to see come down but 0.2% monthly growth is consistent with a 2% path if it holds. In short, today’s print is only one sign of many that the Fed will want to continue to see play out in the coming months. One data point does not make a trend. The preferred view of this data is the three-month annualized trend which is still showing acceleration.

Markets continue to favor a higher rate hike chance of 50 bps instead of 75 bps for the December FOMC meeting while the eurodollar curve shows current market implications of a terminal rate of 5% to peak in March 2023. All of this can quickly change if we’re to see a higher core PCE monthly print for the November data.

Source: Bloomberg, Liz Sonders

Source: BEA

Long-duration Treasurys have rebounded +10.2% from year-to-date lows, after falling -38.65% from historic all-time highs.

While the rebound is notable, we want to continue to highlight the significance in size of the drawdown in U.S. government long-duration debt in inflation-adjusted terms. Shown below is the popular long-term government bond ETF $TLT, with dividends — coupon payments issued by the U.S. Treasury given to you in a fund structure — re-invested, adjusted for the U.S. CPI inflation.

The magnitude of the long-duration debt in REAL terms was, and still is, the biggest story here.

Furthermore, what does this mean going forward for asset valuations?

Below are four previous articles of ours relevant to the matter:

Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle. We think there is a meaningful probability that this is just another bear market rally in global risk assets, as deteriorating economic data is just starting to get priced into conditions.

From a bitcoin-native standpoint, the capitulation has been real. Next week, we will cover bitcoin-specific dynamics including mining, exchanges, on-chain and derivative dynamics.

Thank you for reading Bitcoin Magazine Pro, we sincerely appreciate your support! Please consider leaving a like and letting us know your thoughts in the comments section. As well, sharing goes a long way toward helping us reach a wider audience!