Preview: The FTX Ponzi - Uncovering The Largest Fraud In Crypto History

Modern day alchemy, unsurprisingly, failed. A deep dive into FTX and the events leading to the collapse of the now notorious crypto exchange.

Relevant Past Articles:

This is a preview of “The FTX Ponzi: Uncovering The Largest Fraud In Crypto History”. The full in-depth report has been released to paid-tier Bitcoin Magazine PRO subscribers. If you would like to view the report in full, upgrade your subscription or claim your 30-day free trial of our paid tier.

Beginnings

Where did it all start for Sam Bankman-Fried? As the story goes, Bankman-Fried, a former international ETF trader at Jane Street Capital, stumbled upon the nascent bitcoin/cryptocurrency markets in 2017 and was shocked at the amount of “risk-free” arbitrage opportunity that existed.

In particular, Bankman-Fried said the infamous Kimchi Premium, which is the large difference between the price of bitcoin in South Korea versus other global markets (due to capital controls), was a particular opportunity that he took advantage of to first start making his millions, and eventually billions …

At least that’s how the story goes.

The Kimchi Premium - Source: Santiment Content

The real story, while possibly similar to what SBF liked to tell to explain the meteoric rise of Alameda and subsequently FTX, looks to have been one riddled with deception and fraud, as the “smartest guy in the room” narrative, one that saw Bankman-Fried on the cover of Forbes and touted as the “modern day JP Morgan,” quickly changed to one of massive scandal in what looks to be the largest financial fraud in modern history.

The Start Of The Alameda Ponzi

As the story goes, Alameda Research was a high-flying proprietary trading fund that used quantitative strategies to achieve outsized returns in the cryptocurrency market. While the story was believable on the surface, due to the seemingly inefficient nature of the cryptocurrency market/industry, the red flags for Alameda were glaring from the start.

As the fallout of FTX unfolded, previous Alameda Research pitch decks from 2019 began to circulate, and for many the content was quite shocking. We will include the full deck below before diving into our analysis.

The deck contains many glaring red flags, including multiple grammatical errors, including the offering of only one investment product of “15% annualized fixed rate loans” that promise to have “no downside.”

All glaring red flags.

Similarly, the shape of the advertised Alameda equity curve (visualized in red), which seemingly was up and to the right with minimal volatility, while the broader cryptocurrency markets were in the midst of a violent bear market with vicious bear market rallies. While it is 100% possible for a firm to perform well in a bear market on the short side, the ability to generate consistent returns with near infinitesimal portfolio drawdowns is not a naturally occurring reality in financial markets. Actually, it is a tell-tale sign of a Ponzi scheme, of which we have seen before, throughout history.

The performance of Bernie Madoff’s Fairfield Sentry Ltd for nearly two decades operated quite similarly to what Alameda was promoting via their pitch deck in 2019:

Up-only returns regardless of broader market regime

Minimal volatility/drawdowns

Guaranteeing the payout of returns while fraudulently paying out early investors with the capital of new investors

It appears that Alameda’s scheme began to run out of steam in 2019, which is when the firm pivoted to creating an exchange with an ICO (initial coin offering) in the form of FTT to continue to source capital. Zhu Su, the co-founder of now-defunct hedge fund Three Arrows Capital, seemed skeptical.

Approximately three months later, Zhu took to Twitter again to express his skepticism about Alameda’s next venture, the launch of an ICO and a new crypto derivatives exchange.

“These same guys are now trying to launch a "bitmex competitor" and do an ICO for it. 🤔” - Tweet, 4/13/19

Beneath this tweet, Zhu said the following while posting a screenshot of the FTT white paper:

“Last time they pressured my biz partner to get me to delete the tweet. They started doing this ICO after they couldn't find any more greater fools to borrow from even at 20%+. I get why nobody calls out scams early enough. Risk of exclusion higher than return from exposing.” - Tweet, 4/13/19

Additionally, FTT could be used as collateral in the FTX cross-collateralized liquidation engine. FTT received a collateral weighting of 0.95, whereas USDT & BTC received 0.975 and USD & USDC received a weighting of 1.00. This was true until the collapse of the exchange.

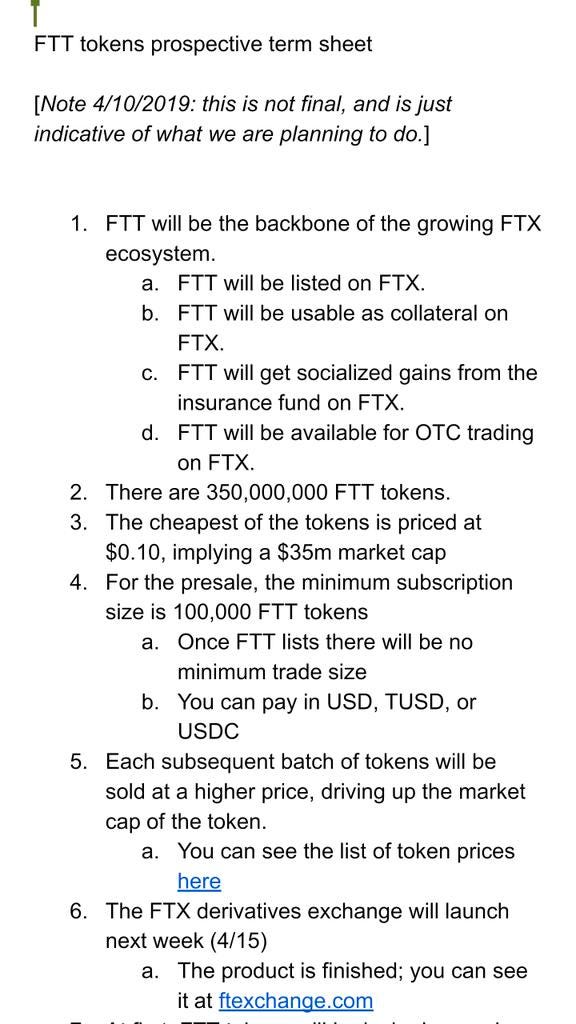

FTT ICO

FTX spun up the FTT token ICO and raised seed rounds for $0.10 and $0.20 while FTX was bootstrapping. Of the 350,000,000 total FTT tokens, the company gifted itself 175,000,000 of the total supply that unlocked over a three-year period.

In particular, as per the FTX website, the 50% premined allocation of FTT that FTX received was meant to be used for the following purposes:

5% - Backstop Fund

Funds set aside in case traders run into bankruptcy.

5% - Safety Fund

Funds set aside in case there are platform losses.

20% - FTT Liquidity Fund

Funds used to provide liquidity in FTT markets.

20% - Team Tokens

Tokens given to project employees.

5% - Adviser Tokens

Tokens given to advisers of FTX.

25% - Company Tokens

Funds locked up over a 3-year period, like the rest of the company tokens.

10% - Ecosystem Fund

Funds used to grow the FTX ecosystem.

10% - User Acquisition Fund

Funds used to help grow the userbase and volume on FTX.

In reality, this was just a long form way of saying that FTX was attempting monetary alchemy; a way of creating nothing from something. When FTT trading launched on FTX, the spot price per token was $0.10 and finished the day trading at $1.60. For the FTX team, they found themselves sitting on hundreds of millions worth of “locked FTT.”

If only they knew that this modern attempt at alchemy would invariably lead to their downfall.

FTT Futures

Interestingly, the FTX team held off on launching FTT perpetual swaps, which was an oddity considering their listing of spot and futures markets for seemingly every other token. Zhu Su once again questioned the delay in launching FTT futures in a series of responses to SBF:

“@SBF_FTX … When do you plan to launch FTT/USDT perps, and any reason for the delay? Might be easier if I just wait for that if it's soon.”- Zhu Su tweet, 7/30/19

“I'd prefer to wait for your FTT/USD derivatives to launch so I can short perps. Is there any ETA on that?” - Zhu Su tweet, 7/30/19

“When will FTT/USD perps launch? That seems like the smoothest way to make this bet, and you already have the tech to launch perps on just about anything. That way the fans can go long also and liquidate my shorts at $4 :)” - Zhu Su tweet, 7/30/19

As we will cover more in-depth shortly, a key feature in the Alameda/FTX scheme was the launch of tokens with extremely bloated FDVs (fully diluted valuations) with low floats at launch. The small amount of tokens that are in circulation are thus extremely easy to pump in price. Similarly, the existence of only a spot market without perpetual swap futures eliminates the ability for others to short and/or hedge their token allocations.

FTT To Directionally Trade

Fast-forward to 2020, and the crypto market has recently gotten obliterated as the March 2020 financial market crash occurred as a result of the pandemic-induced lockdowns. The narrative for bitcoin started to strengthen as the massive fiscal and monetary stimulus that followed the lockdowns had investors looking for a safe haven from monetary debasement. Tangentially, in the land of “crypto,” a phenomenon that later became known as “DeFi Summer'' emerged, whereas the protocols built on Ethereum that allowed for borrowing and lending into pools of collateral emerged. These protocols allowed you to pledge various ETH-based assets as collateral, and borrow stablecoins (or other assets) in return, with variable rates based on the supply and demand for lending.

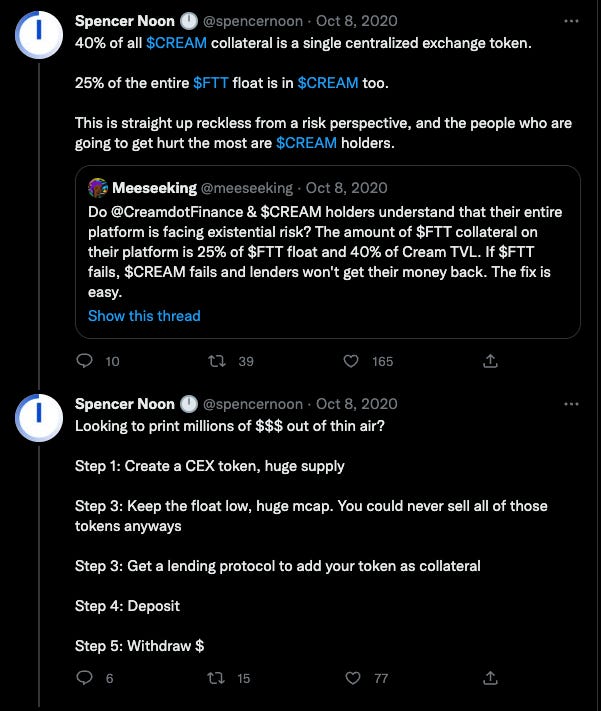

Alameda Research, with FTT collateral that was almost entirely illiquid and owned by themselves, began to use their massive pile of FTT as collateral to short other tokens. Given that there was very little liquidity in FTT, and almost no outstanding float except for their ownership and some owned by friendly VC firms, the token price of FTT itself was nearly impossible to budge.

This dynamic sent alarm bells off throughout the DeFi ecosystem, due to the uncompetitive nature of using your own illiquid exchange token as collateral for directional trading.

Source: Spencer Noon

This was among the first examples of Alameda directionally trading using the FTX exchange token as underlying collateral. Here, you can find a thread of SBF defending these actions (using FTT on Cream Finance to borrow DeFi tokens to short sell) at the time.

The FTX/Alameda Token Model

Source

Another stage in the Alameda/FTX scheme was more monetary alchemy, in the form of their own DeFi ecosystem, built on Ethereum competitor, Solana.

(It should be noted that was announced before the Cream Finance debacle.)

Serum

“Crypto exchange FTX has announced plans to launch a decentralized exchange (DEX), called Serum, built on the Solana blockchain within the next few weeks. FTX CEO Sam Bankman-Fried and crew selected Solana over Ethereum because it’s reportedly more scalable and cost-efficient than its counterpart. But the team intends to integrate a cross-chain gateway between Serum and the Ethereum network that will provide an entry point for current DeFi users to start trading on Serum.” - Messari, 7/20/20

While the supposed advantage of using Solana over Ethereum was one of speed and efficiency, it was clear to outside observers that this was simply a ploy to print tokens out of thin air that could later be sold for an aggressive markup price.

“Of the 10 billion SRM supply, the Serum team and contributors kept 43% and sold 3% in a private sale that has raised ~$7 million to date. The remaining tokens will be split evenly between a collaborator fund and ecosystem incentives fund.” - Messari, 7/20/20

Serum (SRM)’s seed round price for private investors was $0.05, then secondary seed round price was $0.08 to buy a “megaserum.”

Upon listing on FTX, SRM opened at a price of $0.11 and finished the day at $1.55, a massive move that got people talking about the potential for an “Ethereum killer” DEX. SRM continued to pump, reaching $2.70 before its perpetual swap contract was listed on FTX. Serum, similar to many of the other “Sam coins” (in reference to an Alameda/FTX backing) as many began to refer to them as, carried an extremely high fully diluted market cap relative to the current circulating supply. Even today, approximately 3% of SRM’s total supply is in circulation. This is why the existence of perpetual swaps for these tokens is/was so key. With perpetual swaps, locked coins could be initially sold/hedged via short leverage, with any form of underlying collateral.

SRM Current supply relative to its max supply, via CoinMarketCap

FTX/Alameda also aggressively promoted the “assets” OXY and MAPS, both of which had similar dynamics to SRM in terms of its low float/massive fully diluted valuation, along with the launch of spot markets only on FTX (which was an oddity compared to normal FTX operations).

Shown in the screenshot below is the promotion of both OXY, MAPS, and Serum by FTX in late 2020.

Source: Twitter

This concludes the preview of our full report on FTX which has been released to paid-tier Bitcoin Magazine PRO subscribers. If you would like to view the article in full, upgrade your subscription or claim your 30-day free trial of our paid tier.