The State Of GBTC: Discount Shrinks For The First Time In Over A Year

An interesting saga is developing for Digital Currency Group and its Grayscale Bitcoin Trust. Accusations are flying between DCG and Gemini. We analyze GBTC’s current discount to NAV.

Relevant Articles:

The FTX Ponzi: Uncovering The Largest Fraud In Crypto History

The Crypto Contagion Intensifies: Who Else Is Swimming Naked?

The Contagion Continues: Major Crypto Lender Genesis Is Next On The Chopping Block

The State Of GBTC: Discount Shrinks For The First Time In Over A Year

Although it feels like a lifetime ago, only two months have passed since Genesis announced their need for a $1 billion liquidity injection in the aftermath of the FTX and Alameda fallout. In November, we covered initial market risks in “The Contagion Continues: Major Crypto Lender Genesis Is Next On The Chopping Block” and “Digital Currency Group Breaks Silence As Market Hangs In The Balance.”

As weeks dragged on without a resolution, details of the story have become more public, building up to fraud allegations against Digital Currency Group (DCG) that were announced yesterday morning by Gemini co-founder and president, Cameron Winklevoss. Gemini is still trying to recover $900 million in assets from Genesis that were used to generate yield for their Earn customers.

Left unresolved and only growing larger, DCG and Genesis problems weigh heavily on the bitcoin market as there are many answers needed and various possible outcomes that have yet to play out.

The biggest question of all is what will happen to the Grayscale Bitcoin Trust (GBTC) with its extremely low discount that reached 49% and how these issues will potentially impact the bitcoin price. GBTC has been the preferred vehicle for many to obtain regulated bitcoin exposure and it has also been a breeding ground for speculative arbitrage strategies throughout the previous swings going from a premium to a discount to net asset value (NAV). An approved bitcoin spot ETF in the United States would have likely solved these issues, but we’re still far from that happening.

It’s easiest to start with the GBTC shares on DCG’s balance sheet which are estimated to be around 9.67% of the entire supply. In the event that DCG needs to raise cash or goes down the path of Chapter 11 bankruptcy, selling these shares is potentially an option. Selling into an already illiquid market puts more pressure on the historically low GBTC discount. DCG holds approximately 67 million shares in a market that trades less than 4 million shares a day. However, a more important factor is that by law, DCG can sell no more than 1% of shares outstanding every quarter. It would take them around 2.5 years of constant selling to sell their entire stake.

Another path — the most likely one — is that the GBTC, along with Grayscale’s other trusts, find their way into the hands of a new sponsor and manager. Valkyrie has already proposed to do exactly this:

Give an option for investors to redeem shares at NAV through a Regulation M filing request (although it’s not clear a Regulation M request would get approved by the SEC).

Lower fees from 200 basis points to 75.

Attempt to offer investors redemptions in both cash and spot bitcoin.

The option for a new manager gives investors an opportunity to get out of investments at NAV while Valkyrie proposes to pursue a separate Opportunistic Fund which would aim to accumulate GBTC over time until the discount closes.

The GBTC product is still a cash cow for Grayscale and DCG, raking in 2% management fees — in perpetuity. Across all major trust products, Grayscale is collecting over $300 million this year from management fees alone. Rather than liquidate the entire trust in the worst case scenario, there will be many willing buyers to take on management of the vehicle without a U.S. spot bitcoin ETF available in the market.

However, liquidation is not a non-zero possibility. In the event of a Grayscale insolvency or bankruptcy, voluntarily liquidation could be pursued unless 50% of shares vote to transfer to a new sponsor. There is upside to DCG liquidating the trust as there’s money to be made from their shares closing to NAV, but that likely results in selling bitcoin on the open market. No one wants to see 632,000 bitcoin — approximately 3.3% of current supply — become selling pressure in the market. In the unlikely scenario where complete liquidation of the trust is undertaken with USD cash being returned to shareholders, one could presume that much of the selling would be absorbed through OTC deals with interested investors. At this point, this is purely hypothetical.

Based on analysis from Messari, we can see that DCG absorbed all of the previous GBTC sell pressure from BlockFi and 3AC as they offloaded and liquidated positions. DCG has grown their shares by 458% since Q1 2021. If they were to liquidate even a portion of those shares, there’s no current buyer of that size in the market to absorb their selling pressure. Ultimately, that would put further pressure on the current GBTC discount, enticing other shareholders to sell shares as the discount drops further.

(Source)

The rest of this article is open to paying members only. Here’s what’s behind the paywall 🔏:

A closer look at recent developments with the GBTC discount.

How the Grayscale Ethereum Trust plays into these developments.

Some details about an activist campaign brewing among GBTC shareholders. 👀

The GBTC discount saw its largest 1-day positive change since July 2021 on Monday, decreasing the discount to 38.61%. Larger buyers look to be stepping in to bid up GBTC. If the market continues to expect there to be a higher probability that the discount will close, an arbitrage trade here is to buy GBTC shares while shorting bitcoin futures to capture the spread. That’s likely what we’re seeing in the market right now to a certain extent.

The recent decrease in the GBTC discount has coincided with a strong rally across the board for publicly traded companies with bitcoin/crypto exposure. Shares of MicroStrategy, Coinbase, bitcoin miners, and other more illiquid names far outpaced the performance of bitcoin in the recent rally. We suspect that this has played a part in the GBTC discount closing as well — a relief rally following the storm that persisted throughout 2022.

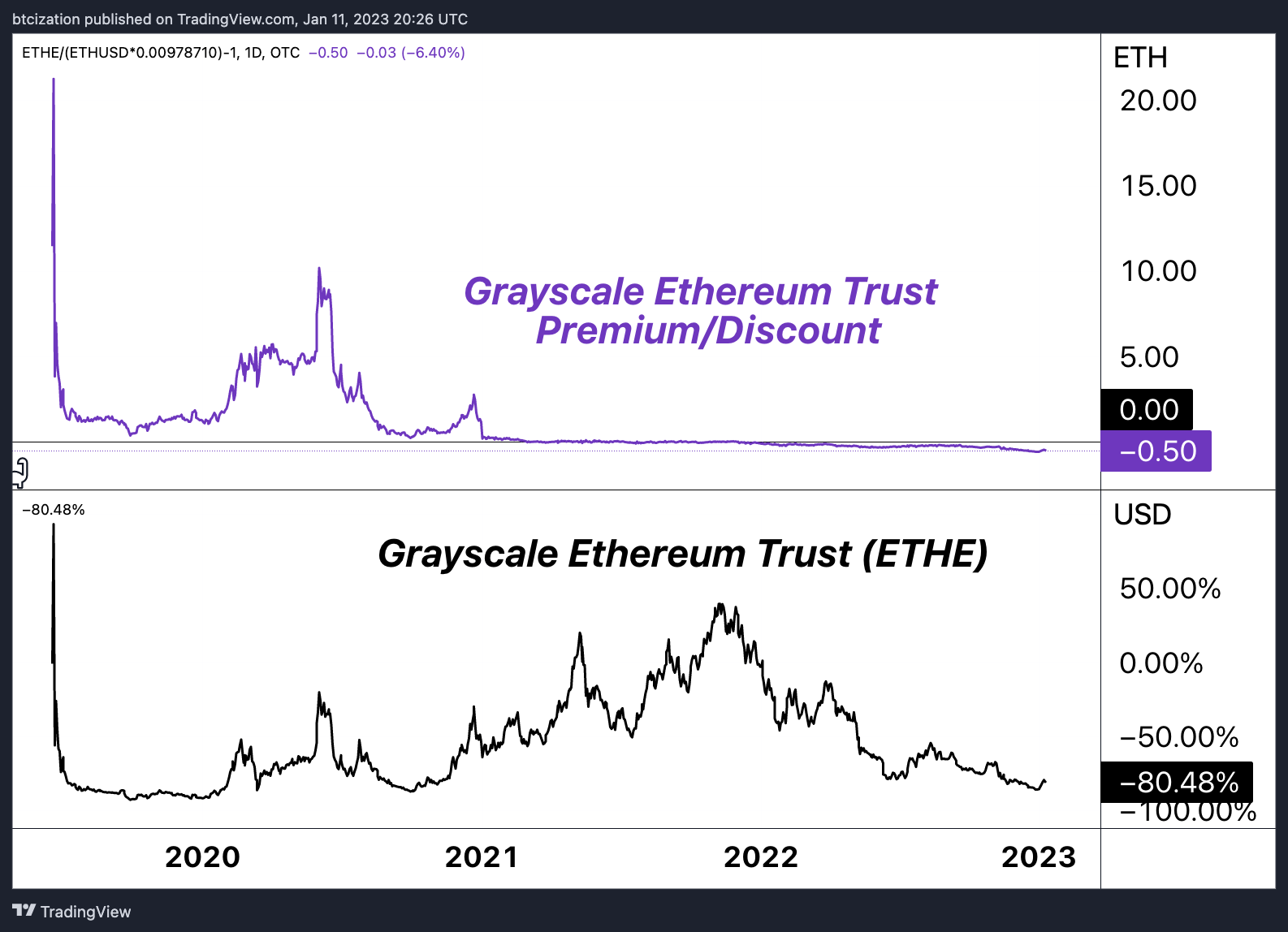

The correlation with the premium/discount to the bitcoin exchange rate is positive to the upside for the first time in over a year, showing that market direction could be serving as a rising tide that is lifting all boats. Similarly, the Grayscale Ethereum Trust (ETHE) — which is approximately 36% of the size of the Grayscale Bitcoin Trust in terms of assets under management in USD terms — has an even larger discount, with shares currently trading -0.49% to NAV.

Given that the ETHE discount has rebounded in tandem with GBTC’s in recent days, we can reasonably suspect that the recent bounce in public crypto vehicles has aided the relative performance.

Final Note

In the coming days, we will be releasing an issue on an activist campaign from GBTC shareholders and include some of the hypothetical paths forward for shareholders of the trust. We will dive into some of the recent allegations against Digital Currency Group from notable actors in the crypto space and what this could mean for the future of Grayscale’s suite of products.

The next article will explore the key role that Digital Currency Group subsidiary Genesis Global played in the meteoric rise of GBTC during the bull run of 2020/2021.

New information coming to light has the potential to change the superstructure in regard to the dynamic between Grayscale and the shareholders of Grayscale products.

Stay tuned for incoming updates.

Thank you for reading Bitcoin Magazine Pro, we sincerely appreciate your support! Please consider leaving a like and letting us know your thoughts in the comments section. As well, sharing goes a long way toward helping us reach a wider audience!