The Unfolding Sovereign Debt & Currency Crisis

Japan’s FX intervention to stop the devaluing yen foreshadows what could happen to the rest of Asia. US dollar continues strengthening. Currencies and sovereign debt yields are bursting at the seams.

Relevant Past Articles

Japan’s Attempt To Rescue The Yen

The U.S. dollar strength saga continues this week with major headline news that Japan is engaging in FX intervention measures to limit the devaluation of the Japanese yen. The last time Japan did this level of intervention was back in 1998 during the Asian Financial Crisis.

This is a unique and extreme measure to stop its currency from bleeding and is likely a temporary solution as currency interventions are rarely successful historically. So far, the yen has seen less than 2% sustained strength on the move this week despite still being down over 20% over the last year.

Working as an opposing force, the Bank of Japan (BOJ) have stuck to their yield curve control guns and are still pinning interest rates to 0.25% with BOJ Governor Haruhiko Kuroda saying,

"There's absolutely no change to our stance of maintaining easy monetary policy for the time being. We won't be raising interest rates for some time."

Japan has the ability to sell a massive amount of U.S. dollars or U.S. Treasurys to the market (in exchange for yen) based on their approximately $1.17 trillion in FX reserves. It’s not exactly known what the mix is between dollars and Treasurys but it’s expected that Japan holds a large amount of cash or cash-equivalents with maturities less than 1 year.

Japan is also the largest foreign holder of the U.S. Treasury securities holding 17.3% of supply just in front of China who is estimated to hold 14.1%.

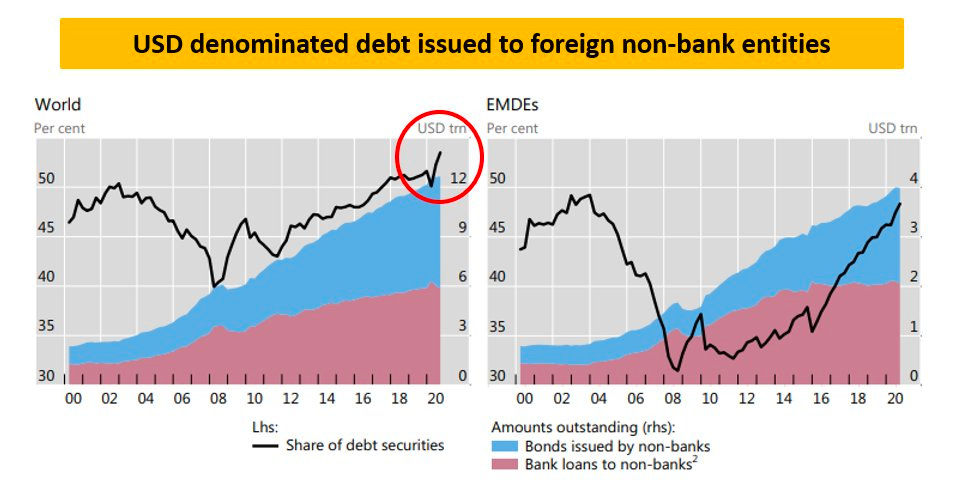

Yet, Japan is not the not only economy facing these monetary policy issues; they are just the red alarm warning sign. Even apart from talking about Europe, emerging market Asian economies are now faced with tough choices on how to weather another currency crisis.

Emerging markets rely on foreign capital to boost economic growth and as a result, must raise interest rates to follow the Federal Reserve’s course to remain competitive in capital markets and limit currency devaluations. Without it, capital would flee these economies and capital controls would be the next wave of policy in order to limit that from happening.

Although the below chart can be hard to see (it’s best to open in another tab and zoom in if you want to see the details), it shows the monthly central bank policy changes around the world from September 2019 to today. Dark blue is lower rate cuts and dark red is higher rate hikes. Every major central bank, apart from Russia and Turkey, are hiking rates at a rapid clip around the world to keep up with the Federal Reserve as there is no other policy alternative.

Source: Mitchel McDonough, Bloomberg

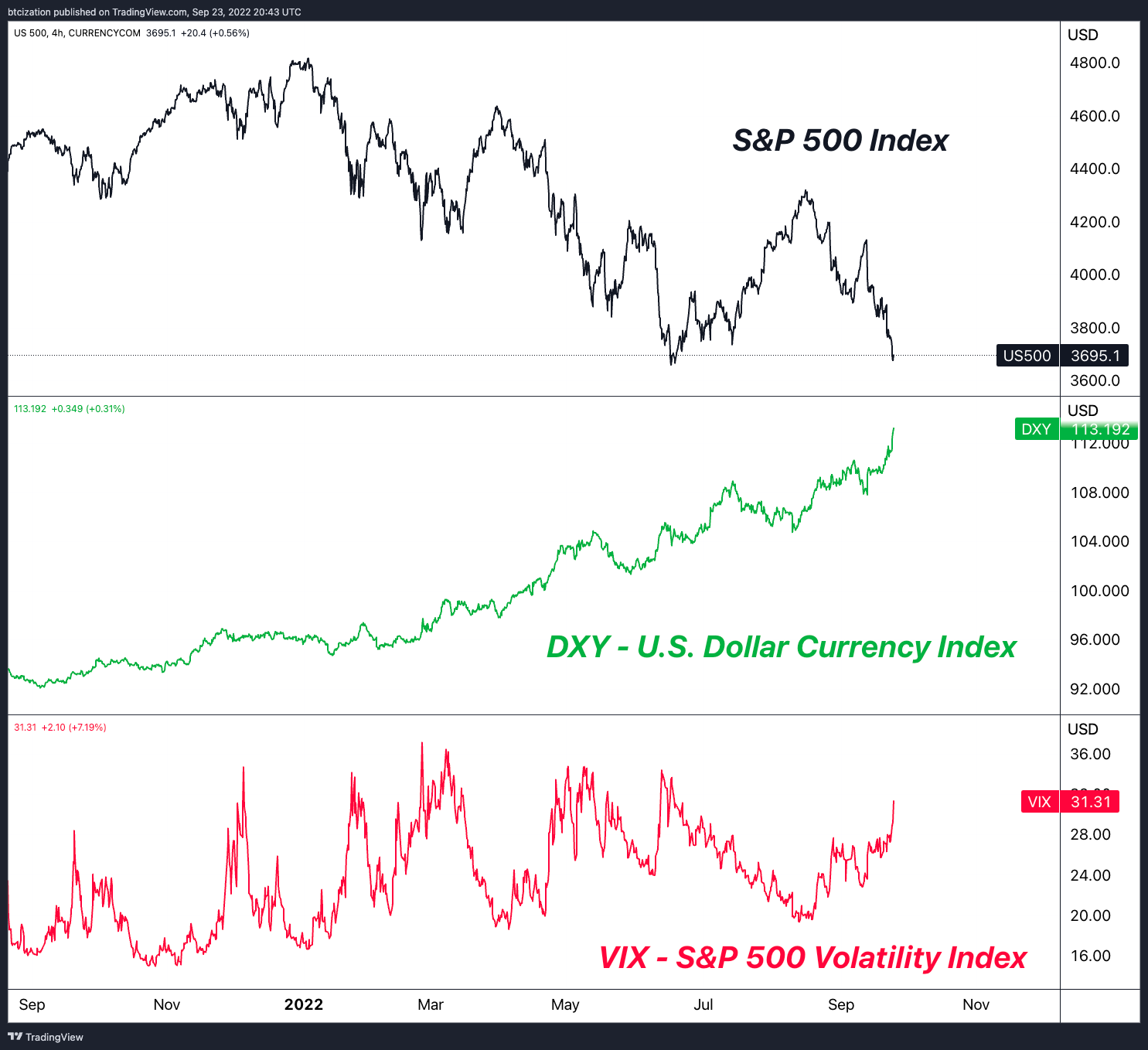

As yields soar across global debt markets, and the Fed rapidly tightens monetary policy, the dollar continues to strengthen, and the global short squeeze strengthens. The euro, Japanese yen, and British pound are all in the process of breaking massively lower against the dollar due to structural forces. Particularly, the strongest force is the international short position of USD, which foreigners are forced to cover by selling currency reserves and/or dollar-denominated assets.

There is a reason why the dollar has risen during every financial crisis/economic slowdown.

Whether the strong dollar is the cause or the effect is irrelevant.

The reason why we continue to nag about foreign exchange and fixed income markets is because the world is currently in the early innings of a funding costs crises, at the household, corporate, and sovereign level. While many people intuitively understand that the endgame of this all will be more monetary stimulus to (attempt) to paper over the cracks, the pain endured getting there could be plentiful.

A debt crisis of this magnitude, at a global scale, occurs with massive volatility.

As energy importing nations deal with balance of payment crises due to the global energy shortage, their currencies are specified as a result, which strengthens the dollar and increasingly puts pressure on dollar-denominated assets in the interim, as USD cash is raised at all cost given the current status of global energy trade.

“There are decades where nothing happens; and there are weeks where decades happen.” - Vladimir Lenin.

Given the size and nature of the sell-off in global debt markets in tandem with a soaring dollar, we look to be living through the weeks where decades happen.

As the Fed aims to enforce its supposed credibility on markets by rapidly tightening the belt in an attempt to clamp down domestic inflationary pressures, its and emerging economies across the globe will be into a deep recession as their currencies and/bond markets collapse. This isn’t a hyperbolic statement; it is happening today.

Thank you for reading Bitcoin Magazine Pro, we sincerely appreciate your support! If you found this article useful, please leave a like and let us know your thoughts in the comments section.