Energy, Currency, & Deglobalization Pt 2; Market Reacts to Jackson Hole

The second in a two-part series on the changing world order, its impacts on the global economy, and the future of central bank monetary policy. Plus, an update on the Fed's Jackson Hole conference.

Special Announcement

We have some exciting changes coming to Bitcoin Magazine PRO!

It is our goal to provide you with the best possible insights to navigate the market and to do that, we believe it is important to have skin in the game.

With this in mind, we are happy to announce the addition of Dr. Jeff Ross who will be managing the new Bitcoin Magazine PRO Fund beginning in early September!

Dr. Jeff has extensive experience managing capital through his firm Vailshire Capital Management and is a highly-respected voice in the Bitcoin space. He will be making long/short calls, actively managing risk, and giving you actionable trade ideas, all while updating you on the performance of the Bitcoin Magazine PRO Fund.

Paid subscribers will receive these updates, in-depth market commentary from our research team, and will continue to receive early access to our monthly market research reports as they are released.

We will continue to release details as the launch approaches, thank you for supporting Bitcoin Magazine PRO!

Today’s issue is the second leg of our two-part issue, “Energy, Currency, & Deglobalization.” For subscribers who have not yet read yesterday’s issue, please read that first for context on the topics and issues discussed previously.

As we covered the brewing geopolitical tensions and developing energy crises in Europe in yesterday’s issue, let's cover some of the possible second order effects, as well as outline our short-term and long-term market outlook, with quotes from the ever-insightful Zoltan Poszar from his latest piece “War and Industrial Policy.”

Before diving back into the big ideas from Poszar, let’s review the market moves today following Federal Reserve Chairman Jerome Powell’s speech at Jackson Hole.

As Powell began to speak, global markets began to sell off sharply, with equities quickly making new lows, as bitcoin followed in tandem while the dollar rallied. Shown below are the three respective charts (with DXY inverted). For now, it’s all one trade (more on this later).

Among the most interesting developments in recent weeks has been the divergence between the bond market and the equities market, as yields across the curve continued to push higher in tandem with equities, which is not a relationship that is expected to last.

All else being equal, higher yields equal higher discount rates and borrowing costs, and when the largest market in the world (bonds) is selling off significantly, equities can only swim against the tide for so long.

The repricing in yields was in part due to the rise in Fed Funds expectations in 2023, with a significant amount of repricing taking place over the course of recent weeks towards higher rates for longer. In fact, that was one of the key talking points in Powell’s speech today.

The Fed has been fairly transparent about their intent to raise interest rates to combat inflation, and today was no different.

Powell even went further today, so much as to admit “pain” is likely to be felt by households and businesses,

"While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses” - Jerome Powell

As said in our July Monthly Report: “Long Live Macro,”

“The story of 2022 has been the inflation-induced monetary tightening that has occurred across financial markets. In an attempt to fulfill their dual mandate of price stability and full employment (more on this later), the Federal Reserve has embarked upon one of the fastest hiking cycles in history.”

The combination of tightening monetary policy globally coupled with a structural energy shortage has led to the dollar strengthening against other fiat currencies materially.

“A strong dollar is in the process of completely upending the global economy. While there are certainly exogenous factors that are causing the economic pain points such as shattered supply chains following COVID-19 economic lockdowns (which were incredibly strained following unprecedented levels of monetary and fiscal stimulus in 2020/2021) and the Russia/Ukraine conflict which has thrown global energy and commodity markets in flux, a strong dollar only increases pressure on foreign nations in terms of meeting their dollar-denominated liabilities, while increasingly harming U.S. domestic industry.” - “Dollar Go Up: Global Macro Headwinds Intensify, 7/15/22”

Let’s return to the excellent work of Zoltan Pozsar before further examining the likely path for financial markets and Fed policy:

“Globalization is not a bank in need of a bailout. It’s in need of a hegemon to maintain order. The systemic event is someone challenging the hegemon, and today, Russia and China are challenging the U.S. hegemony. For the current world order and its trade arrangements and network of global supply chains to survive the challenge, the challenge must be squashed quickly and decisively, in the spirit of the Powell Doctrine.

“But Ukraine and Taiwan aren’t Kuwait, Russia and China aren’t Iraq, and ‘Top Gun 2’ isn’t the same movie as ‘Top Gun’ … Think about what Tim Geithner said about how to deal with crises like the Asian financial crisis or a herd of short sellers questioning the solvency of the U.S. banking system. In today’s context, Russia and China are basically the ‘short sellers.’”

To be able to attempt to outcompete Russia and China, the U.S. desperately needs to reshore domestic manufacturing. This not only takes time, but plenty of raw materials and infrastructure, all of which are inflationary. Yes, the Fed is attempting to destroy demand (at the margin) to combat inflation, but during “wartime,” industrial policy and economic sovereignty take importance.

“I get it why the U.S. wants to invert time. But we can’t win by slowing progress. We’ll also have to progress by building, and that’s where industrial policy comes in: as an investor, you care about the inflationary consequences of Russia and China challenging the U.S. hegemon. Where inflation goes, policy rates go, or if not, financial repression is an issue.”

“Either way, you care, especially if you are a bond house or if you depend on fixed income. These are the scary times when the ‘euthanasia of the rentier’ is a risk. To ensure that the West wins the economic war – to overcome the risks posed by ‘our commodities, your problem’; ‘chips from our backyard, your problem’; and ‘our straits, your problem’ - the West will have to pour trillions into four types of projects starting ‘yesterday’:

(1) re-arm (to defend the world order)

(2) re-shore (to get around blockades)

(3) re-stock and invest (commodities)

(4) re-wire the grid (energy transition)

“I think that the above four themes (re-arm, re-shore, re-stock, and re-wire the electric grid) will be the defining aims of industrial policy over the next five years. How much the G7 will spend on these items is an open question, but given that the global order is at stake, they will likely not be penny pinching. If Tim Geithner were in charge, he’d put ‘a lot of money in the window’ to show who’s in charge.

“And hopefully it will be like that … and if so, any investor will have to be mindful that the above to-do-list is:

commodity intensive

capital intensive

interest rate insensitive

uninvestable for the East

“Commodity intensity means that inflation will be a nagging problem as the West executes on the above list. Re-arming, re-shoring, re-stocking, and re-wiring need a lot of commodities – it’s a demand shock. It’s a demand shock in a macro environment in which the commodities sector is woefully underinvested – a legacy of a decade of ESG policies.

“Capital intensity means that governments and also the private sector will have to borrow long-term to execute the to-dos. Re-arming and re-stocking are the domains of the government, and re-shoring and re-wiring the grid will involve public-private partnerships. Private firms will have to issue debt and raise equity to build things: ships, F-35s, factories, commodity warehouses, and wind turbines. Insensitivity to interest rates means that the to-do-list will have to be executed regardless of whether the Fed hikes rates to 3.5% or 7%. Hell or high water, executing on the to-do-list is imperative.

“Finally, uninvestability means that for certain large countries in the global East, it makes absolutely and categorically no logical sense to roll their investments in G7 debt claims. Not just because of what happened to Russia’s FX reserves, but also because rolling a $1 trillion portfolio of U.S. Treasury securities means that you will fund the West’s effort to re-arm, re-shore, re-stock, and re-wire … against the East.”

You don’t think it's a coincidence that China is persistently selling its stash of U.S. Treasurys, do you? After seeing what happened to Russia, and the latest military operations off the coast of Taiwan, China looks to be preparing for increased hostility with the West. This isn’t a call nor even a prediction of war, but rather observations that likely are too aligned to be merely coincidental.

Takeaways

Let's go over what we’ve covered so far:

An economic crisis is developing in Europe, with energy rationing a likely outcome for many this winter as shortages are prevalent.

Energy importer nations are facing rapid currency devaluation

Yields on global debt are skyrocketing across the board as central banks attempt to fight supply side inflationary pressures with demand destruction

As weak currencies depreciate against the dollar and trade slows due to skyrocketing energy prices, dollars are increasingly hard to come by to fulfill denominated liabilities, leading to further dollar strengthening

The conditions and sovereign cooperation which enabled the disinflationary environment of the last three decades is rapidly reversing, and the left tail risk of escalating geopolitical tension is real

Due to a matter of national security, the U.S. government will likely need to spend/invest massive amounts of money to reshore domestic manufacturing, during a time where finance costs have rapidly risen

As a result, the market is likely pricing in a near best case scenario outcome of softening inflationary pressures

As Powell and the Federal Reserve are emboldened to tighten policy into a global slowdown, with the dollar strengthening to new highs on a weekly basis and energy prices skyrocketing around the world, we view it as increasingly likely that something breaks in a massive way over the next six months. Six months may even be too generous of a timeline.

Given the Fed plans to begin quantitative tightening next month, reducing its balance sheet to the tune of $95 billion per month, we expect something under the surface will crack in financial markets.

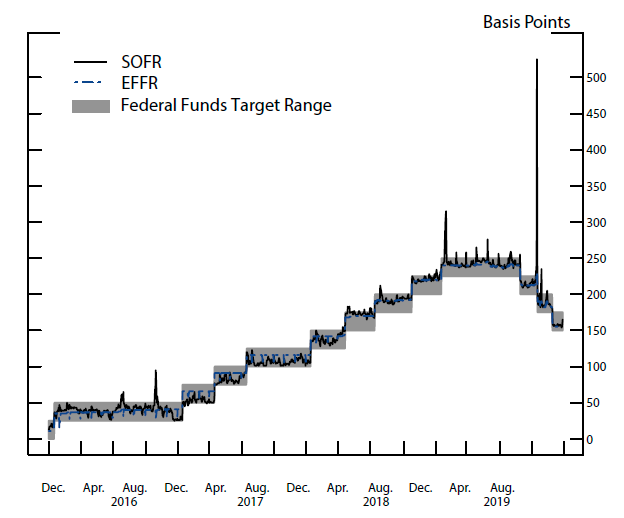

Remember the last time the Fed attempted to strategically reduce its balance sheet, in 2019?

As the Fed rolled off its balance sheet, overnight money markets seized up and SOFR (secured overnight financing rate), a measure of borrowing costs for borrowing against treasuries skyrocketed far above the target rate set by the Fed.

The repo market broke.

The Fed responded by once again expanding its balance sheet, and notoriously emphasizing that the expansion should not be thought of as “quantitative easing.”

While liquidity conditions are entirely different today, the macro headwinds faced today are nearly an order of magnitude more complex and challenging than those faced back in 2019.

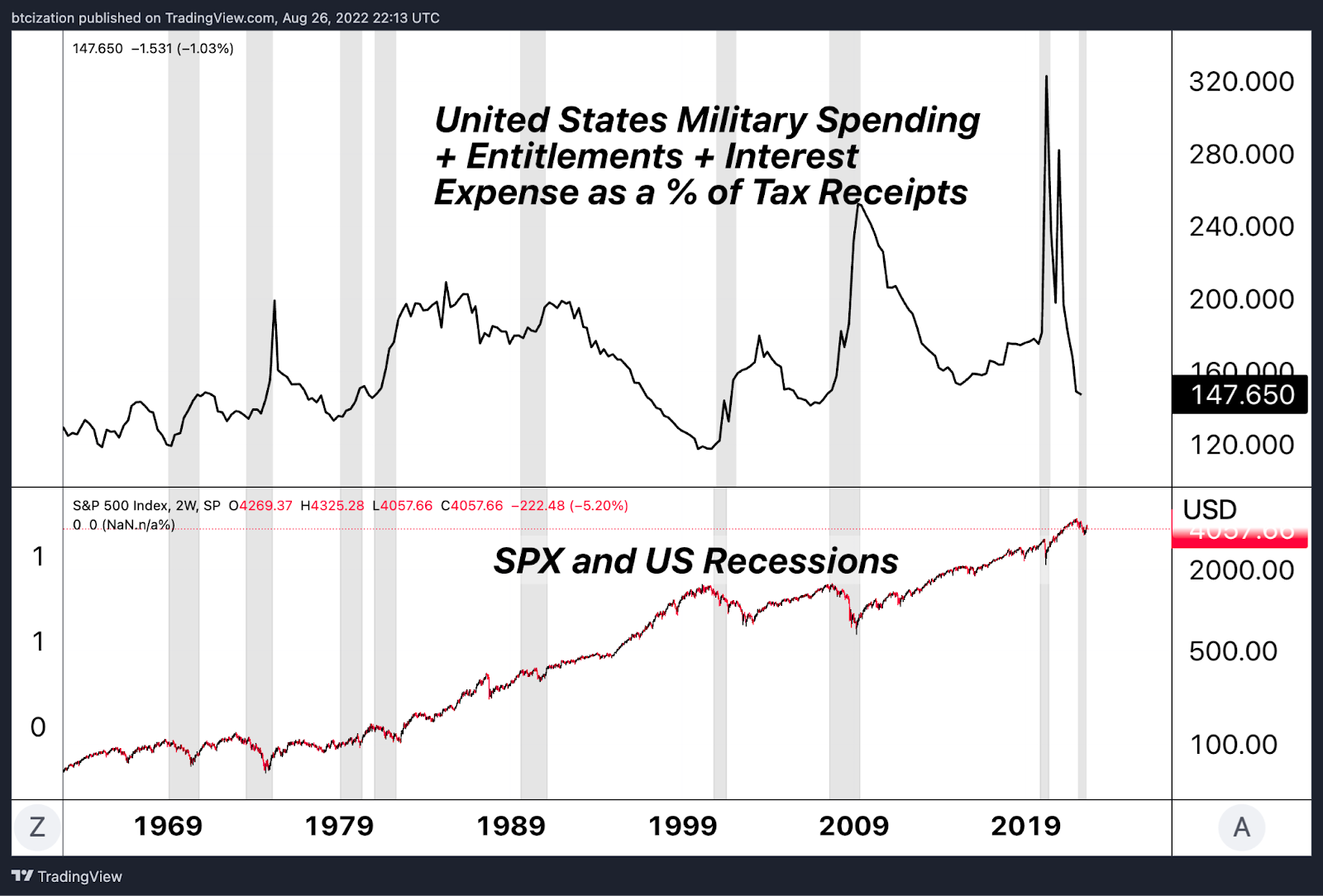

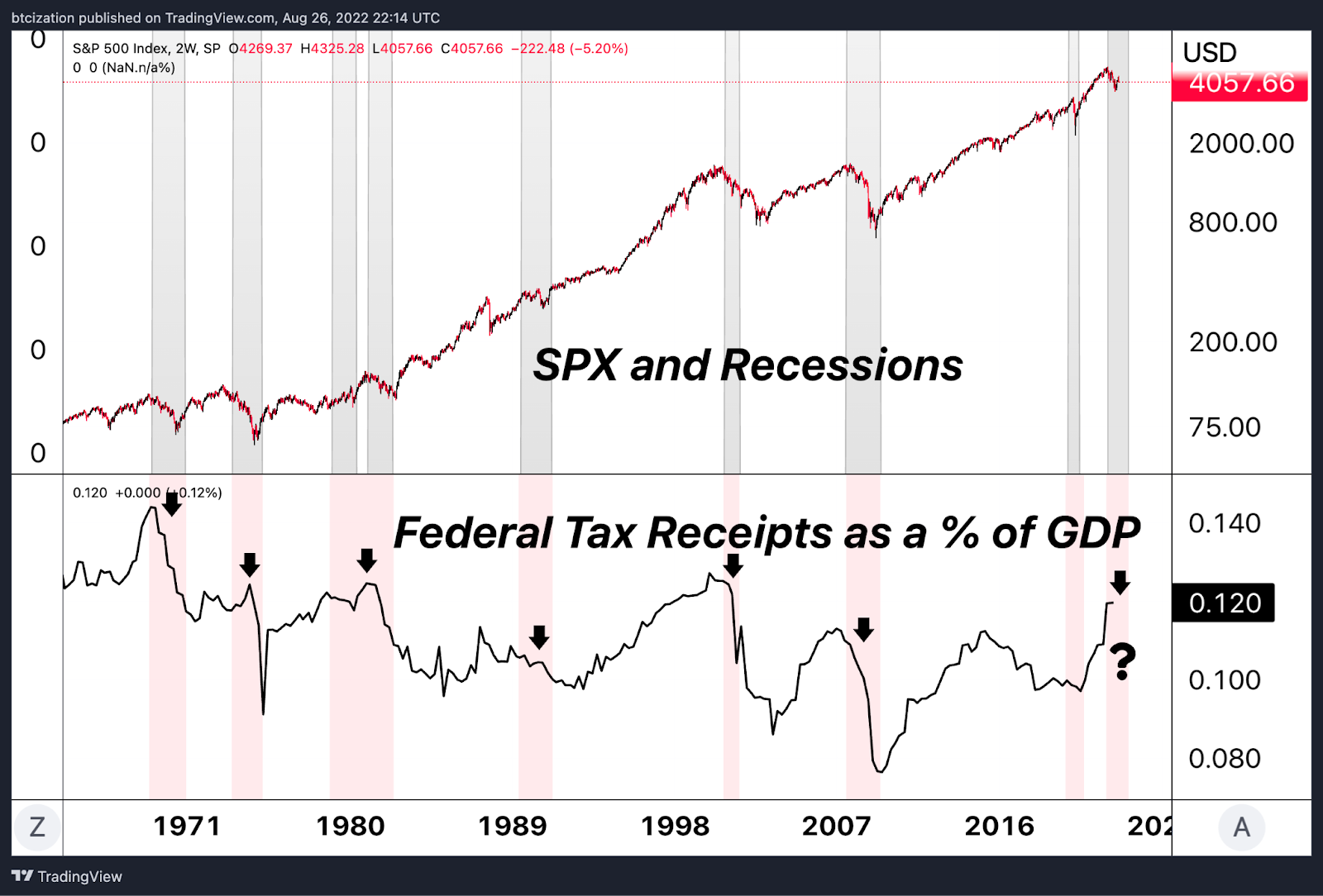

As covered extensively in our July Monthly Report, the Fed is tightening policy while the U.S. Treasury spends more than 140% of tax receipts on necessities. Not to mention the fact that during recessionary periods, tax receipts fall markedly (as a result of falling asset prices).

With this being said, we think what “breaks” is liquidity in the U.S. Treasury market, as a soaring dollar, skyrocketing energy prices and subsequently contracting global productivity lead to a sell-off in dollar-denominated assets.

There still is a massive implicit short dollar position around the world (USD-denominated debt).

We still have yet to see the blow-off top short squeeze in the USD. In that environment only two places are safe, volatility (as an asset class) and dollars. Everything else sells.

Bitcoin won't be insulated, nothing will.

When that time comes, the Fed will be forced to print into an inflation spike.

This is when bitcoin comes back with a vengeance.

Thank you for reading Bitcoin Magazine Pro, we sincerely appreciate your support! If you found this article useful, please leave a like and let us know your thoughts in the comments section.

can you give a price range of what you think the upcoming cycle bottom will be?

Jeff Ross is dope. Great to hear he is going to manage the fund! Also, great article! Time to yeet these markets!