July Monthly Report Preview: Long Live Macro

Become a premium subscriber to Bitcoin Magazine PRO to get access to the July monthly report and all of the Bitcoin Magazine PRO research. We will release the full report to free subscribers this Saturday, August 6th.

Sign up with the button below to get a 30-day free trial premium subscription and access to the full report today.

PREPARED BY:

Dylan LeClair, Head of Market Research

Sam Rule, Lead Analyst

Summary:

Long Live Macro

Risk Parity Correlation, Recession

Inflation, Federal Reserve Policy

Global Indicators, Eurodollar Curve

Government Spending

Spending Percentage Of Tax Receipts

Hyper-Financialization

Net Worth, Negative Real Yields

Equities

Compressed Valuations

Rising U.S. Dollar Risk

Earnings Projections, PMI Slowdown

Illiquidity And Volatility

Credit Spreads, Unemployment

Extreme Tail Risks

Central Bank Balance Sheets

Introducing: Bitcoin

Days Below Realized Price

Put/Call Options, Perps Funding

Global M2 Growth

Executive Summary

With 2022 well past the halfway point, it is abundantly clear that long/short macro investing has come back with vengeance. Riding high following the stimulus-frenzied market of 2020/2021, 2022 has been characterized by soaring inflation, hawkish central bank monetary policy, cratering asset prices and increasing geopolitical tension between economic superpowers.

The contents of this report will dive into the dynamic macroeconomic landscape, which will use a multidimensional approach to analyze financial markets and economic data.

Long Live Macro

The story of 2022 has been the inflation-induced monetary tightening that has occurred across financial markets. In an attempt to fulfill their dual mandate of price stability and full employment (more on this later), the Federal Reserve has embarked upon one the fastest hiking cycles in history.

While this is a bitcoin-focused publication, the contents of this report will extensively cover many different developing macroeconomic trends, with the purpose of gaining a more comprehensive understanding of the global financial market landscape, which we will then use to evaluate probable future outcomes, which will in turn bring us back to bitcoin and the potential future performance thereof.

On Thursday July 28, it was announced that the United States economy contracted by 0.9% in real terms during the second quarter, marking the second consecutive quarter of negative gross domestic product (GDP) growth, and officially entering the economy into a technical recession (despite the denial by certain key political parties and figures). A deceleration and an eventual outright contraction of growth became an increasingly obvious outcome during the first quarter of 2022 as prices of key commodities, particularly energy, soared causing interest rates to fly and central banks to reverse course from their policies of easing to net tightening. Notably, stocks and bonds held an extremely strong positive correlation for long periods of time during the sell-off, which hadn’t occurred since the inflationary bear market of the 1970s.

In a previous issue of Bitcoin Magazine Pro released on March 7, 2022, titled Rising Commodities And Flattening Yield Curve, we stated the following.

“It would be wise to warn our readers that despite being extremely bullish on bitcoin’s prospects over the long term, the current macroeconomic outlooks looks extremely weak. Any excessive leverage present in your portfolio should be evaluated…

“…Indiscriminate selling of bitcoin will occur (along with every other asset) in a rush to dollars. What is occurring during this time is essentially a short squeeze of dollars.

“The response will be a deflationary cascade across financial markets and global recession if this is to unfold.”

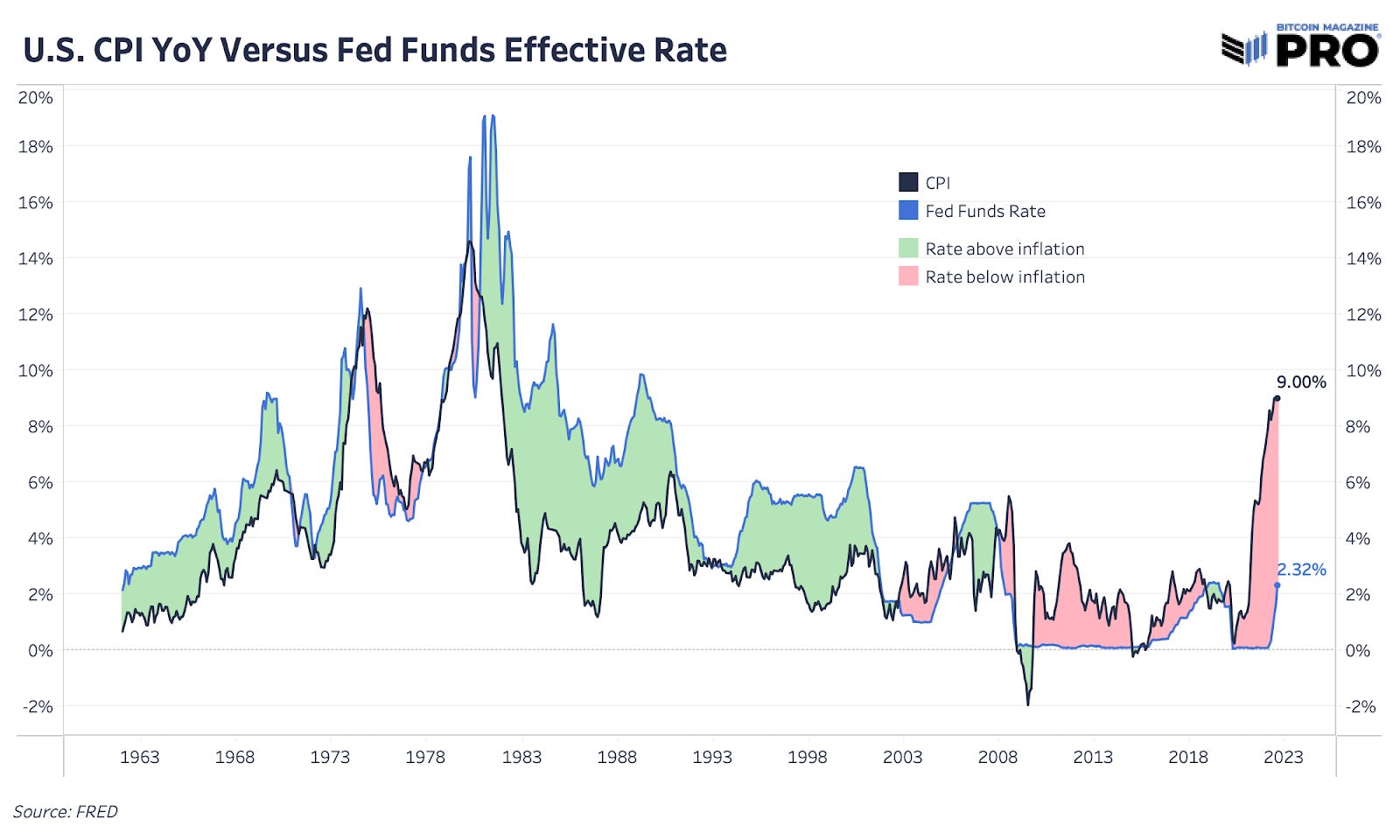

Nearly five months later, risk assets have puked, the Federal Reserve has raised their target rate by a total of 225 basis points over the course of the last four FOMC meetings, year-over-year consumer price index (CPI) inflation has accelerated to a politically unpalatable 8.99%, and the dollar has strengthened materially against other major global currencies.

Is the bottom in risk assets in, or is the bullish price action merely a classic bear market rally? Let’s examine, with specific focus on the following asset classes: equities, fixed income, yields, volatility, commodities, foreign exchange, real estate and lastly, bitcoin and cryptocurrencies.

The most important dynamic to understand is that the Federal Reserve (and other global central banks of less importance) only have one tool to fight structural inflation: monetary policy. While the optimal solution to a fundamental supply/demand imbalance would be to increase supply through CapEx (capital expenditures) investments from commodity producers, the Federal Reserve is working to instead kill demand to bring down prices in an attempt to fulfill its dual mandate of maximum employment and stable prices.

Stated another way, the Fed is purposefully embarking upon a mission to punish asset prices and weaken U.S. economic activity in an attempt to curb inflation. Fed Chairman Jerome Powell is stating the Fed’s goals quite clearly.

In the latest FOMC meeting on Wednesday July 28, Powell said the following,

“We actually think we need a period of growth below potential in order to create some slack so that the supply side can catch up.”

“We also think that there will be, in all likelihood, some softening in labor market conditions.”

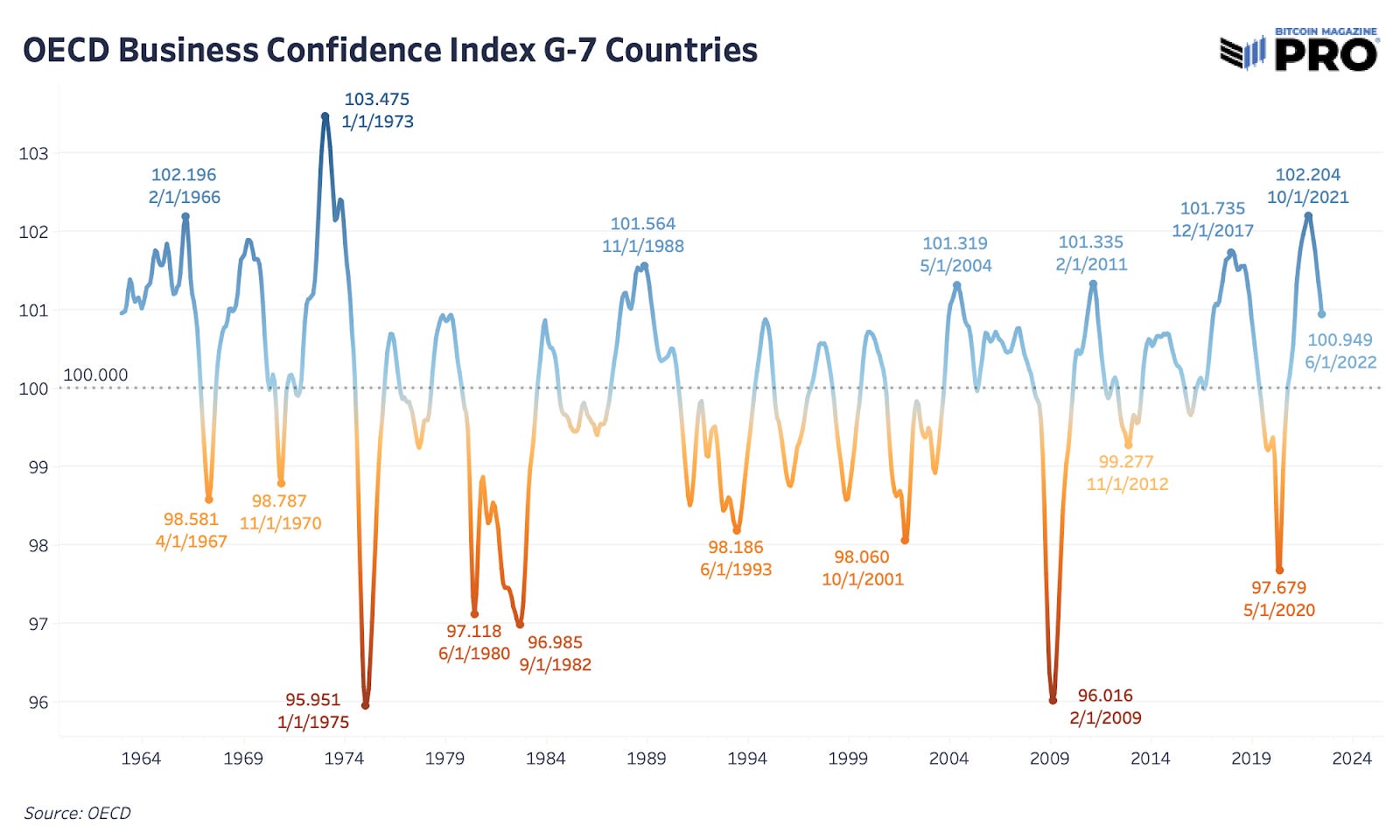

The good news for the Federal Reserve is that the slowdown in growth is coming. The bad news is that it is coming, fast. Across G-7 countries, business confidence is rolling over meaningfully while consumer confidence in many countries is at its lowest reading in recorded history. The consumer has gotten pillaged as a result of the spiraling inflationary pressures.

Shown below are U.S. hourly earnings in real terms, showing that workers in the U.S. have seen their compensation reduced in real terms even while wages are fast rising in nominal terms.

As the Fed has tightened, the bond market has begun to price in a significant slowdown in growth and call the Fed’s bluff, as Treasury bonds yields have fallen below the respective yields offered on Treasury bills, as the market is pricing in the dynamic of inflation today at the expense of a long-term slowdown in real growth.

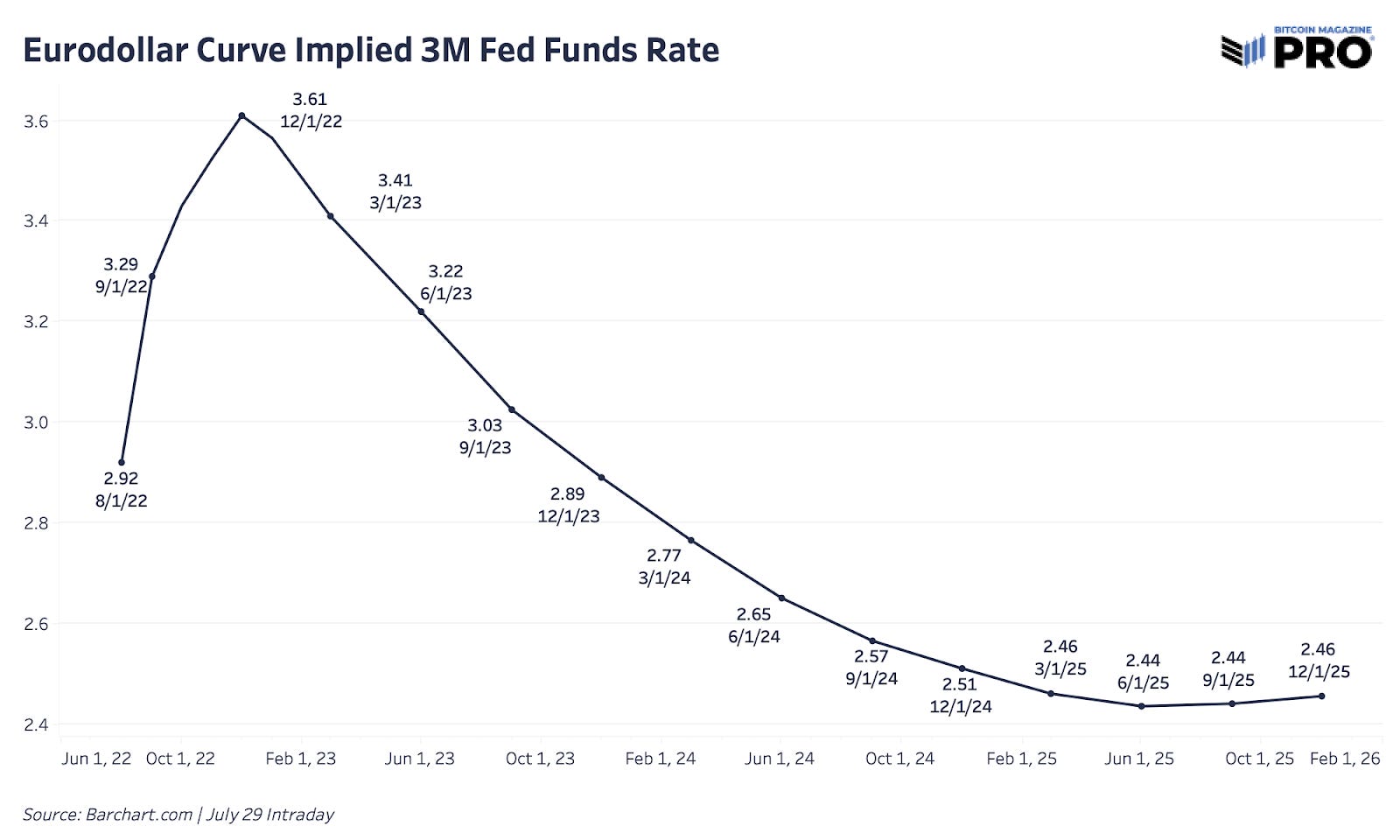

Similarly, eurodollar futures, a market for future Fed funds rate has severely inverted into 2023, with the market’s expectations for long-term rates to settle around 2.5%, more than 100bps lower than expectations for rates in December.

Let’s revisit the reason why this is the case. Why does the market so strongly believe that the Fed cannot sustain high rates for long? The short answer/s to the question is as follows:

Sustained periods of high interest rates will functionally bankrupt the U.S. government;

U.S. entitlement spending (Social Security and the Department of Health and Human Services) plus military spending plus interest expense accounted for 149% of tax receipts for the fourth quarter of 2021.

For context, 149% was the number during a time when short-term interest rates were below 1%, tax receipts were at all-time highs (due to bloated financial markets), and before COLA (cost of living adjustments for entitlement programs) was raised by 5.9% at the end of 2021 (future estimates for 2023 COLA adjustment are approximately 8%).

As a thought experiment, think of the U.S. government as a business that entered the year 2022 spending $149 for every $100 it earned in income on just the bare minimum essentials. On top of this, the business has a debt-to-income ratio of 124%. To make matters worse, as the year has progressed, interest rates have soared, future income (in the form of tax receipts) are guaranteed to fall due a lack of harvestable capital gains, and inflation has further increased the size of annual expenses (in the form of entitlements which can be thought of as off-balance-sheet IOUs, otherwise known as unfunded liabilities).

Now, we know that the Keynesian economic model is built upon the concept of governments and central banks using fiscal and monetary policy during business cycle downturns to ease the burden on individuals and institutions. Empirical evidence of this phenomenon can be seen by looking at previous recessionary periods in U.S. economic history over the last five decades. During the last eight recessions, spending on the “essentials basket” (entitlements, defense budget, and Treasury interest expense) increased in nominal terms by an average of 23.79% from the official start of the recession until six months after the official “conclusion” of real growth contraction on average.

Similarly, median spending by the U.S. government on the “essentials basket” increased by a median amount of 24.79% from the official start of the recession until six months after the official conclusion of real growth contraction.

Now with that in mind, notice the relationship between recessionary periods and spending as a percentage of tax receipts during and directly following the period.

Notice a trend?

This is the end of the preview for the July 2022 Long Live Macro Report. The full report will be released to free subscribers Saturday, August 6th. Subscribe so you don’t miss out!