The Daily Dive #074 - Shift Towards Cash-Margined Bitcoin Futures Continues

Increasing Cash-Margined Futures Market

In the Daily Dive #028 we covered the structural shifts in the bitcoin derivatives market, and what it meant for future price action and market structure. Today’s Daily Dive will provide an update on this trend shift.

Since the April local market top, the bitcoin derivatives market has witnessed a secular shift towards an increasingly cash (dollar/stablecoins)-margined futures market, instead of the previously predominant bitcoin-margined market (70% of total open interest on April 17, 2021).

This shift is significant for a number of reasons. With all else being equal, an increasingly cash-margined futures market means that long liquidations are significantly less likely and common compared to recent history, as well as short squeezes being increasingly more likely compared to recent history.

This is because of the relationship between the two forms of collateral and price. With bitcoin as derivative market collateral, when the price draws down the value of the underlying collateral declines in tandem in a convex relationship that leads to sharp drawdowns and massive market liquidations for leveraged longs. Conversely, with dollars/stablecoins as derivatives collateral, short squeezes are increasingly common because as the price of bitcoin increases, it takes an increasing amount of cash to cover the margin short position, resulting in increasingly large short squeezes the more dominant cash-margined derivatives become in the market ecosystem.

While some of the shift can be attributed to a rise in cash-margined open interest, the sharp decline in aggregate bitcoin-margined open interest is the reason for the structural shift, and this has occurred across all derivatives exchanges. The significant falloff in the percentage of bitcoin-margined futures open interest was largely driven by Binance activity with the rest of key exchanges across Bybit, Huobi and OKEx (exchanges that offer both bitcoin and stablecoin-margined contracts) remaining over 50%.

Due to the natural bull bias held by bitcoin/crypto traders, using cash/stablecoins as collateral is unequivocally preferable, thus it should serve as no surprise that this development has continued to occur.

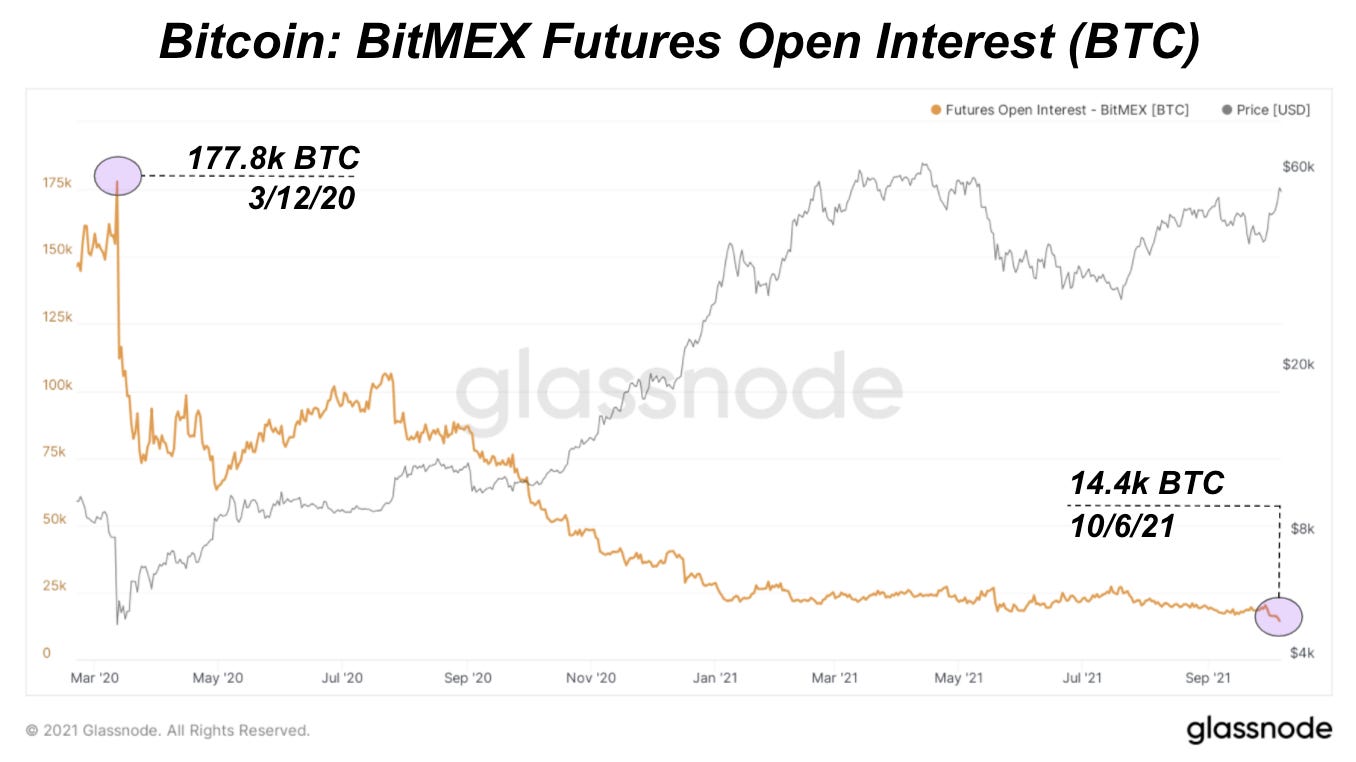

It also should be mentioned that the fall of BitMEX has played a significant role in altering the derivative market structure. BitMEX, which founded the notorious perpetual swap futures contract in 2016, was one of the largest derivative exchanges by volume for an extended period of time, but the March 2020 derivatives blow-up, the indictment of the original founders in October 2020, mandatory KYC for users (recent development over the last year) and the gradual shift of preference towards cash-margined futures has led open interest on the platform to drop by more than 90% in BTC terms.