The Daily Dive #056 - Cracks In The Legacy System Continue To Arise

The cracks in the legacy system continue to arise. The monetary environment globally is truly unprecedented, and as we have reiterated many times in the past in The Deep Dive, we believe this is the final crack-up boom of the great fiat monetary experiment.

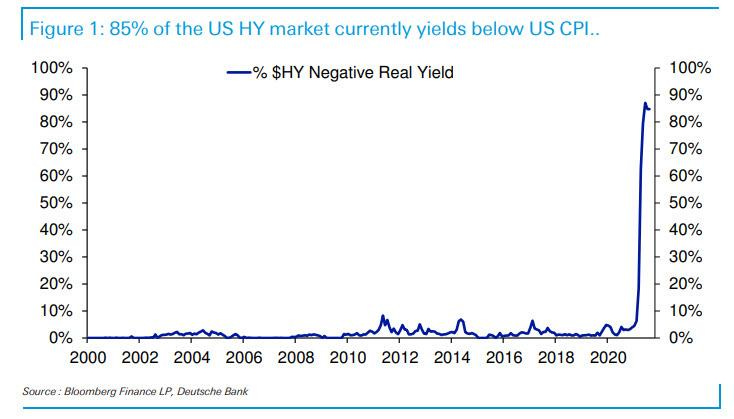

Deutsche Bank's Jim Reid recently published staggering numbers regarding the U.S. high-yield bond market, as shared by ZeroHedge. With Debt/GDP at such elevated levels, and with the Federal Reserve committed to let inflation run hot, and with the Consumer Price Index inflation at 5.4%, and the index of high yield bonds yielding 3.87%, in total 85% of the bonds in the U.S. high-yield market currently carry a negative real yield. Even if CPI dropped 240 basis points to 3% year over year, 35% of the high-yield market would still have a negative real yield.

Relatedly, in an article published on Monday in Bloomberg, it was reported that real yields on a basket of junk debt went negative for the first time ever as consumer prices hit decade highs.

This isn’t a Eurozone or U.S.-centric “problem.” This is what the tail end of a 80-year debt supercycle looks like. The crumbling monetary order that was first established in 1944 at Bretton Woods, which devolved into a full-on global fiat experiment in 1971 is in the end game.

As debt has continued to accrue across all economic sectors and demographics, the universal response has been easier money for decades. Now with debt at unacceptable levels across the globe, the answer is financial repression.

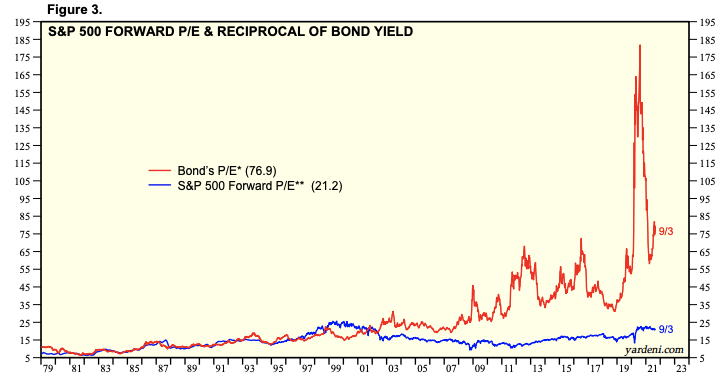

Next, let's examine bond yields along with forward price to earnings (P/E) of S&P 500 equities since 1979. Notice the correlation break that occurred in the late 90s, as the monetary policy from the late Greenspan days aimed at blowing asset bubbles for the wealth effect.

The often misunderstood thing about bonds is the convexity that occurs with a trip towards the zero-lower bound. The P/E of a bond is the inverse of the yield, and as rates held toward zero the forward P/E explodes, due to the convexity.

Below is the S&P 500 “fair value” when using the 10-year Treasury bond yield as a benchmark. As the cost of capital is pushed towards zero, and in real terms *negative*, the fair value of an equity is theoretically infinity. Now obviously that is hyperbolic, but at a time when governments are increasingly running deficits completely financed by central bank monetization while consumer inflation readings jump to the highest level in decades, equities are being treated like safe havens where bonds are fair to protect investors.

The cost of capital is broken. This needs to be repeated.

Ultimately, this is not something that can be easily dealt with. Kicking the can during a 40-year secular asset boom by lowering the cost of capital is the easy part. The hard part comes when the cost of capital can no longer be lowered (in nominal terms).

This is what the final crack-up boom of fiat currency looks like.

A broken and manipulated cost of capital? Yeah, you guessed it. Bitcoin fixes this.