The Bitcoiner's Guide To Yield Curve Control & The Fiat End Game

Yield Curve Control: the next saga in the global monetary policy experiment. From the US's 1942 implementation to Japan’s recent endeavor, what is yield curve control and what are its consequences?

Relevant Past Articles

Here Comes Yield Curve Control

A key theme in our long-term Bitcoin thesis is the continued failure of centralized monetary policy across global central banks in a world where centralized monetary policy will likely not fix, but only exacerbate, larger systemic problems. The failure, pent up volatility and economic destruction that follows from central bank attempts to solve these problems will only further widen the distrust in financial and economic institutions. This opens the door to an alternative system. We think that system, or even a significant part of it, can be Bitcoin.

With the goal to provide a stable, sustainable and useful global monetary system, central banks face one of their biggest challenges in history: solving the global sovereign debt crisis. In response, we will see more monetary and fiscal policy experiments evolve and roll out around the world to try and keep the current system afloat. One of those policy experiments is known as yield curve control (YCC) and is becoming more critical to our future. In this post, we will cover what YCC is, its few historical examples and the future implications of increased YCC rollouts.

YCC Historical Examples

Simply put, YCC is a method for central banks to control or influence interest rates and the overall cost of capital. In practice, a central bank sets their ideal interest rate for a specific debt instrument in the market. They keep buying or selling that debt instrument (i.e., a 10-year bond) no matter what to maintain the specific interest rate peg they want. Typically, they buy with newly printed currency adding to monetary inflation pressures.

YCC can be tried for a few different reasons: maintain lower and stable interest rates to spur new economic growth, maintain lower and stable interest rates to lower the cost of borrowing and interest rate debt payments or intentionally create inflation in a deflationary environment (to name a few). Its success is only as good as the central bank’s credibility in the market. Markets have to “trust” that central banks will continue to execute on this policy at all costs.

The largest YCC example happened in the United States in 1942 post World War II. The United States incurred massive debt expenditures to finance the war and the Fed capped yields to keep borrowing costs low and stable. During that time, the Fed capped both short and long-term interest rates across shorter-term bills at 0.375% and longer-term bonds up to 2.5%. By doing so, the Fed gave up control of their balance sheet and money supply, both increasing to maintain the lower interest rate pegs. It was the chosen method to deal with the unsustainable, elevator rise in public debt relative to gross domestic product.

Yet by 1947, inflation was over 17% (measured by year-over-year consumer price index) and the Fed was growing concerned about the YCC’s impact on inflationary pressures so they stopped YCC on the short-term bills. Inflation came surging back in 1951, over 21% annualized, and YCC on longer-term bonds was ended despite opposition from the current presidential administration and fiscal policymakers to keep it going. The Fed was actually the one fighting to end YCC efforts here highlighting,

“With inflation on the rise, the FOMC felt strongly that the continuation of the peg would lead to excessive inflation.”

Fast forward to today, YCC came back to the main stage as a tool for both Japan and Australia in 2016 and 2020 respectively. Japan has been setting the short-term policy rate and the 10-year rate at varying levels over the years to actually try and spur inflation around 2%. It wasn’t until April of this year, when global inflation pressures were soaring, that Japan was able to get their core inflation rate over 2%.

This year, we’ve seen Japan face a serious decision on maintaining their YCC policy: allow yields to rise or the Japanese yen to fall. Rising yields seem an unsustainable option with Japan having the largest public debt-to-GDP ratio in the world, around 260%, while facing a multi-decade issue to spur sustainable economic growth and inflation.

Currency devaluation is the other side of the sword though with a sustained YCC policy. As a result, the yen now looks more like an emerging market currency down 20% year-to-date. It has now swung too far for comfort and the Bank of Japan (BoJ) has gone full-on FX intervention mode to limit the bleeding, even if it's only going to prove to be temporary relief. The yen losing some of its value can benefit competitive imports and economic growth, but losing too much will destroy domestic purchasing power. We seem to be in yet another example of central banks finding out their policies are more of a runaway on/off switch and less of a calculated dial.

Source: Bianco Research

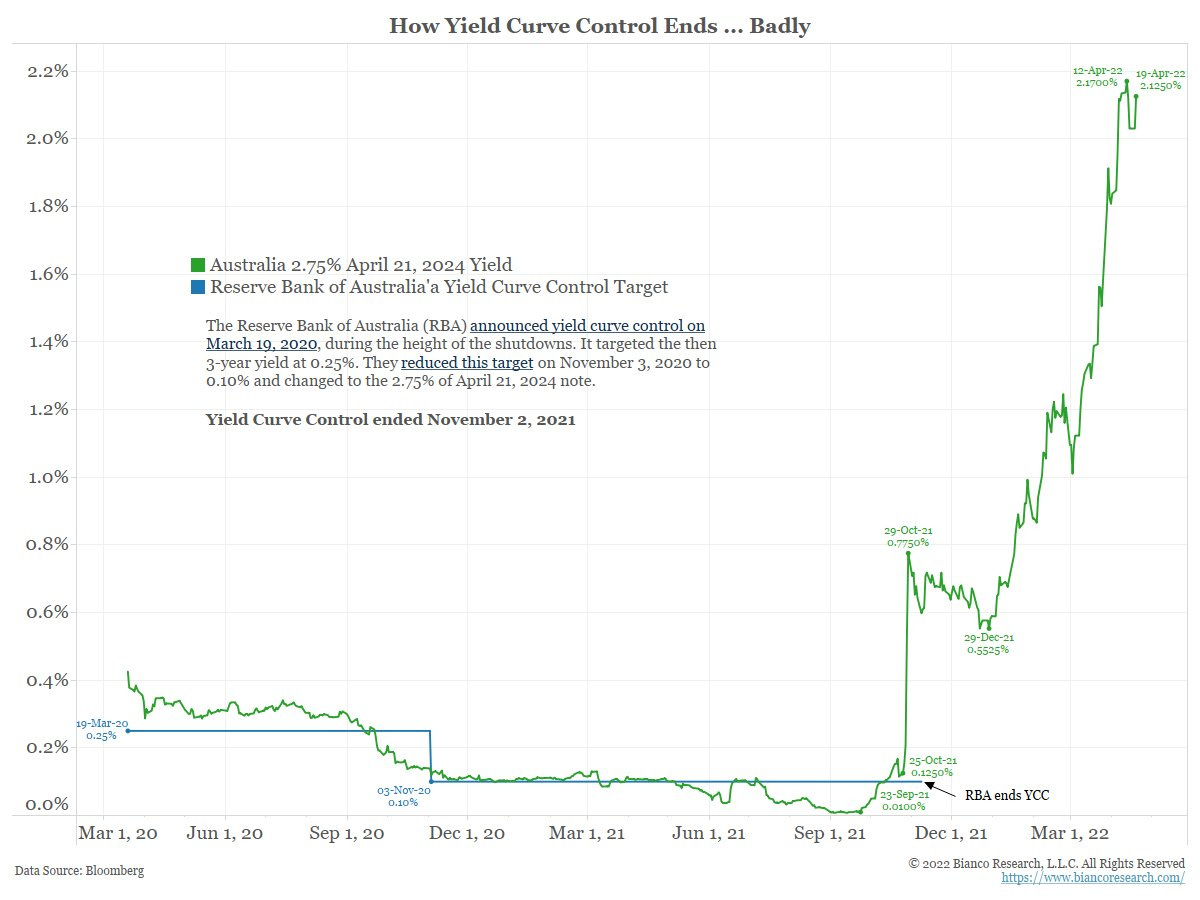

In the heat of the pandemic, Australia rolled out an interest cap on 3-year bonds at 0.1% in an effort to stimulate the economy and assure their citizens that interest rates would remain low and stable until 2024. Amidst rising inflation, bond markets called their bluff and pushed the rate to 0.8% which completely forced the Reserve Banks of Australia (RBA) to end the program. Overall, consensus is that the YCC attempt was a failure as the RBA had no real exit plan to stop the policy as rates started to rise.

Source: Bianco Research

YCC Current And Future

Apart from these clear YCC examples, the European Central Bank (ECB) has effectively been engaging in a YCC policy flying under another banner. The ECB has been buying bonds to try and control the spread in yields between the strongest and weakest economies in the eurozone.

This bond buying has evolved into what is now called the anti-fragmentation tool or “transmission protection instrument” (TPI). The policy is designed to buy and sell various bonds across EU countries to try and cap yields in hopes to stop a sovereign debt crisis or large-scale default from happening. The spread between Italian and German debt is one of the best examples to show why the ECB is concerned and feels compelled to roll out drastic action.

Announced just this morning, the Bank of England (BoE) took action to restart pseudo quantitative easing (QE) efforts amidst concerns that major pension funds were facing insolvency and margin calls as yields continue to rip higher. U.K. 10-year yields were 1% at the start of the year and reached a peak of 4.58% before turning over on the new policy news. 30-year yields in the U.K. reached as high as 5.12% before moving sharply lower on the announcement of Bank of England intervention. The move, one of absolutely massive proportion in global bond markets, saw the value of the 30-year gilt rise by as much as 28.57% in approximately four hours.

Yields have become too high too quickly for economies to function and there’s a lack of marginal buyers in the bond market right now as sovereign bonds face their worst year-to-date performance in history. That leaves the BoE no choice but to be the buyer of last resort. If the QE restart and initial bond buying isn’t enough, we could easily see a progression to a more strict and long-lasting yield cap YCC program.

From the BoE’s own words, bond purchases will continue on whatever scale is necessary, which sure does sound a whole lot like a new regime of YCC forming. It’s reminiscent of Mario Draghi’s “whatever it takes” moment during the European debt crisis in 2009.

“To achieve this, the Bank will carry out temporary purchases of long-dated UK government bonds from 28 September. The purpose of these purchases will be to restore orderly market conditions. The purchases will be carried out on whatever scale is necessary to effect this outcome. The operation will be fully indemnified by HM Treasury.”

Source: Bloomberg

It was later reported that the BoE stepped in to stem the route in gilts due to the potential for margin calls across the U.K. pension system, which holds approximately £1.5 trillion of assets, of which a majority were invested in bonds. As certain pension funds hedged their volatility risk with bond derivatives, managed by so-called liability-driven investment (LDI) funds. As the price of long-dated U.K. sovereign bonds drastically fell, the derivative positions that were secured with said bonds as collateral became increasingly at risk to margin calls. While the specifics aren’t all that particularly important, the key point to understand is that when the monetary tightening became potentially systemic, the central bank stepped in.

Returning to the intervention itself, the initial scale of this operation is relatively small and isn’t a direct sign that a global pivot is going to play out tomorrow. Inflationary pressures are still enemy number one, especially in the United Kingdom which has projected inflation to 9.5% through 2023. The British pound is also exploding with volatility, down over 20% year-to-date. Surely every country with energy import concerns and high inflationary pressures is keeping an eye on Japan’s YCC efforts and currency path as a warning sign for how things can worsen.

Although YCC policies may “kick the can” and limit crisis damage short-term, it unleashes an entire box of consequences and second order effects that will have to be dealt with.

For starters, the rising inflationary pressures that can come from YCC are difficult to predict even in the more deflationary world we find ourselves in today. With inflation rampant and policy goals to destroy it, increased YCC could easily lead us into a world of more inflationary shocks, not less.

YCC is essentially the end of any “free market” activity left in the financial and economic systems. It’s more active centralized planning to maintain a specific cost of capital that the entire economy functions on. It’s done out of necessity to keep the system from total collapse which has proven to be inevitable in fiat-based monetary systems near the end of their shelf life.

YCC prolongs the sovereign debt bubble by allowing governments to lower the overall interest rate on interest payments and lower borrowing costs on future debt rollovers. Based on the sheer amount of public debt size, pace of future fiscal deficits and significant entitlement spending promises far into the future (Medicare, Social Security, etc.), interest rate expenses will continue to take up a greater share of tax revenue from a waning tax base under pressure.

As we’ve also seen with many monetary policies over the last decade, governments continue to increase their share of global debt markets crowding out private investment. What becomes the incentive for private investors to purchase sovereign debt if yields and returns are capped? Investors likely end up only holding government debt because they are forced to across various regulatory and capital control policies.

Final Note

The first use of yield curve control was a global wartime measure. Its use was for extreme circumstances. So even the attempted rollout of a YCC or YCC-like program should act as a warning signal to most that something is seriously wrong. Now we have two of the largest central banks in the world (on the verge of three) actively pursuing yield curve control policies. This is the new evolution of monetary policy and monetary experiments. Central banks will attempt whatever it takes to stabilize economic conditions and more monetary debasement will be the result.

If there was ever a marketing campaign for why Bitcoin has a place in the world, it’s exactly this. As much as we’ve talked about the current macro headwinds needing time to play out and lower bitcoin prices being a likely short-term outcome in the scenario of serious equity market volatility, the wave of monetary policy and relentless liquidity that will have to be unleashed to rescue the system will be massive. Getting a lower bitcoin price to accumulate a higher position and avoiding another potential significant drawdown in a global recession is a good play (if the market provides) but missing out on the next major move upwards is the real missed opportunity in our view.

Thank you for reading Bitcoin Magazine Pro, we sincerely appreciate your support! Please consider leaving a like and letting us know your thoughts in the comments section. As well, sharing goes a long towards helping us reach a wider audience!

This financial climate is beginning to resemble the 'slowly then all of a sudden' reaction activity all over the world!

Who cracks first?

How does Japan do it?!

Your analysis is quite valuable Dylan & Sam!

I often look forward to reading your well thought out work at the end of the day 👍🏻

Master class with this one. Impressive run down compiled here of YCC background and recent state of play.