Today’s issue will be covering the latest developments in the bitcoin derivatives market. For frequent readers of Bitcoin Magazine Pro, you are familiar with how closely we follow the derivatives landscape and just how significant its dynamics are to the bitcoin price over the short/intermediate term.

While it is clear today that the dominant driver in the bitcoin market is its correlation to equity markets, we believe that a true decoupling will take place eventually, and the seeds of that decoupling likely could be sown in the derivatives market.

First off, a major development over the last two years has been the “dollarization” of collateral type in the derivatives market, eliminating much of the downside convexity that comes with a majority of collateral being bitcoin itself.

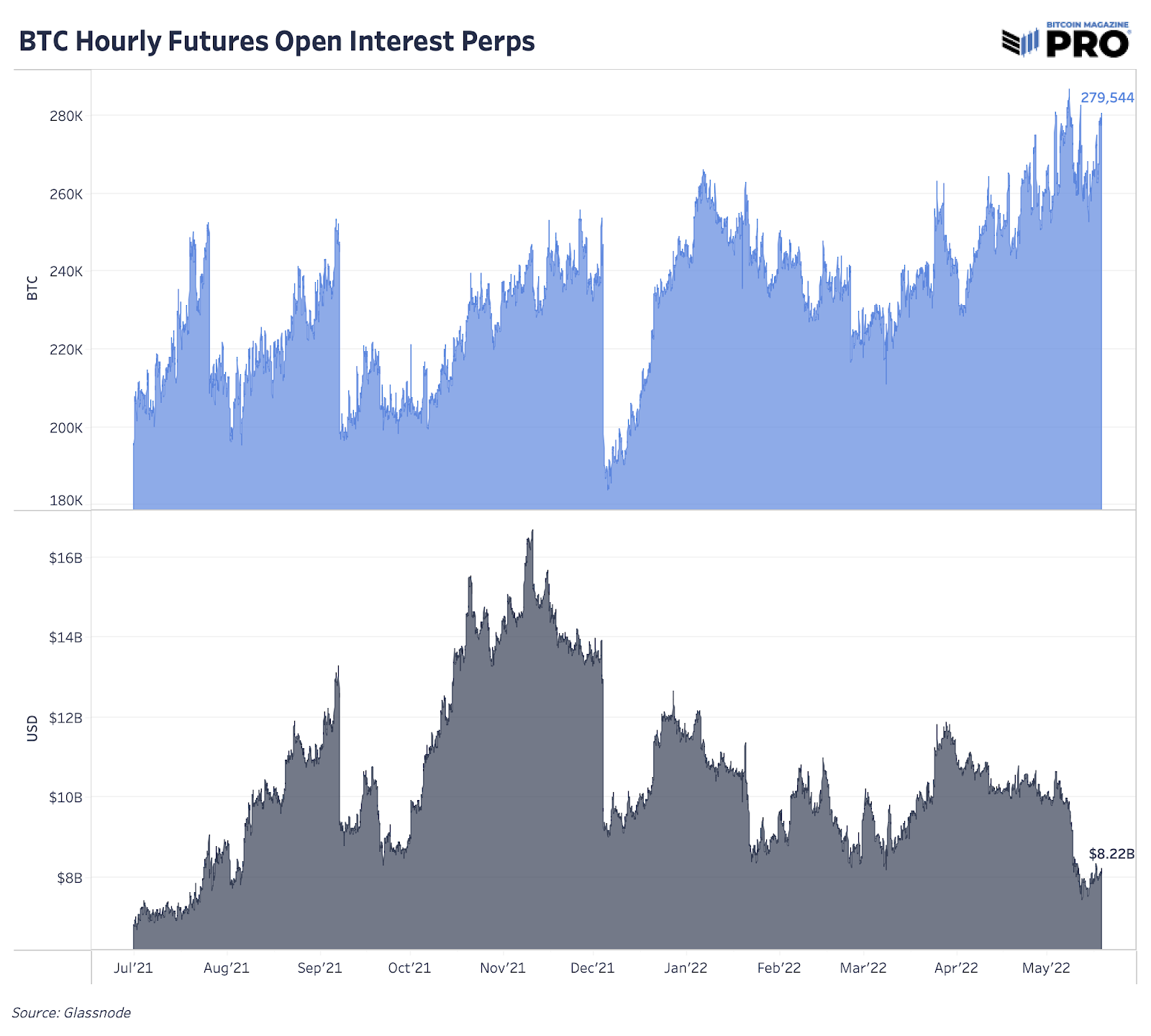

With 56.72% of open interest being collateralized with dollars, the market is increasingly likely to face large short squeezes if bearish derivative traders get offside.

We covered this scenario in our January 21st release,

“A look at the perpetual futures funding rate, which is positive or negative depending on where the contract is trading relative to the spot bitcoin market, displays this dynamic:

Cascading liquidation events drive bitcoin derivative contracts far below the spot price, which is why funding goes negative following large long liquidations.

It needs to be reiterated that everything is probabilistic in nature, and nothing is a sure thing to occur, but if the stock market sell-off worsens, a framework similar to the March 2020 event will likely do you well.”

While a large liquidation event in the bitcoin market is less likely than March 2020 based purely on the collateral makeup in the market today as well as the positioning of the contracts (shown below), it is clear that global equity and credit markets are in free fall. With this in mind, and the reality that spot markets have absorbed a massive amount of selling pressure in recent weeks, one would be wise to keep a close eye on the derivatives market going forward.

While the funding rate on perpetual swaps has been flat/slightly negative, we have yet to see sustained periods of deeply negative readings, which is one of the telltale signs of a bitcoin macro bottom.

Open interest in bitcoin terms is historically elevated, but with neither bulls nor bears having a large appetite for risk, neither side has found themselves too far offside in recent weeks.

Final Note:

The Federal Reserve is on a mission to reverse engineer the infamous wealth effect, with the idea that falling asset prices will dampen consumer confidence and spending, and slow down the unprecedented inflation being witnessed around the world.

If global markets are headed for a breaking point, you can expect bitcoin to face steep pressure as well. What isn’t known is how many bitcoin investors/speculators are still in the market left to panic, and whether the selling that would come would be through spot markets or more predominantly through shorting via bitcoin derivatives.

In either scenario, it is likely that a horde of bottom shorters will pile on attempting to drive bitcoin into the dirt (this will be able to be seen via a deeply negative perpetual futures funding rate).

This will eventually lead to a large rebound in the price of bitcoin, and likely a decoupling/outperformance of other risk assets that have been so tightly correlated with bitcoin in recent months.

Opportunity lies ahead.

Dylan, Sam, you guys rock. Great synopsis. Keep on stackin, and keep some dry powder for a major capitulation. I'm out of ammo. Couldn't help myself in the low 30's and even bought some more in the high 20's. I'm broke Ha