BM Pro Daily - GBTC, BITO And MicroStrategy

Bitcoin Investment Vehicles

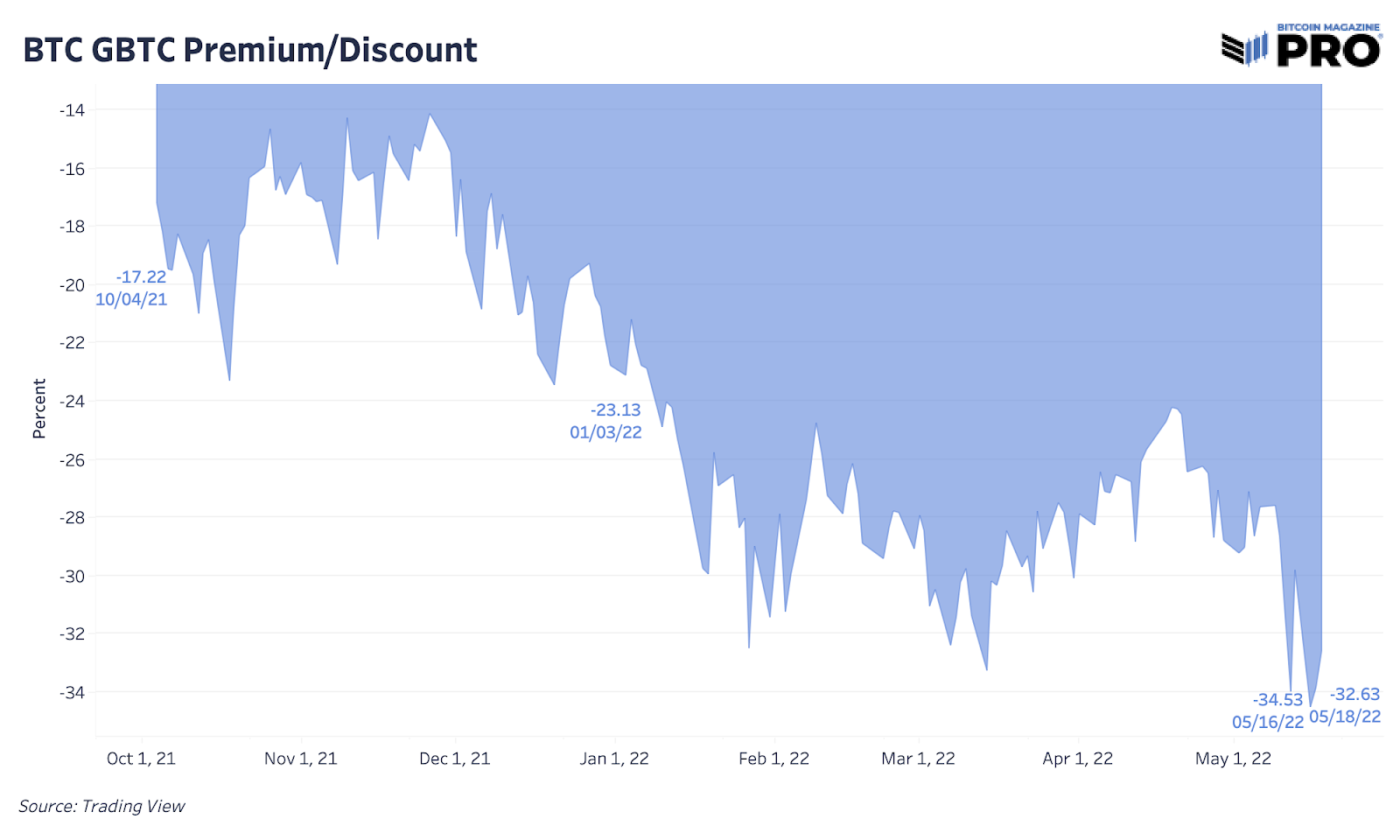

In our issue last month, GBTC Discount Shrinks, we highlighted the latest state of the Grayscale Bitcoin Trust, an overview of its spot ETF approval process and expected 2023 timeline. At that time, we were seeing a reversal in the GBTC discount trading at 23.15% up from its 30% low.

Since then, the discount has dropped further, reaching an all-time low of 34.5% this week. Likely this steepening discount is a result of more market sell-offs in risk appetite and the market’s reaction to the LUNA UST market blowup. Although the failure of LUNA can be thought of as strengthening the case for Bitcoin long-term (the best will survive), this example will certainly be used as firepower for increased government regulation, scrutiny and investor protection efforts across the entire industry.

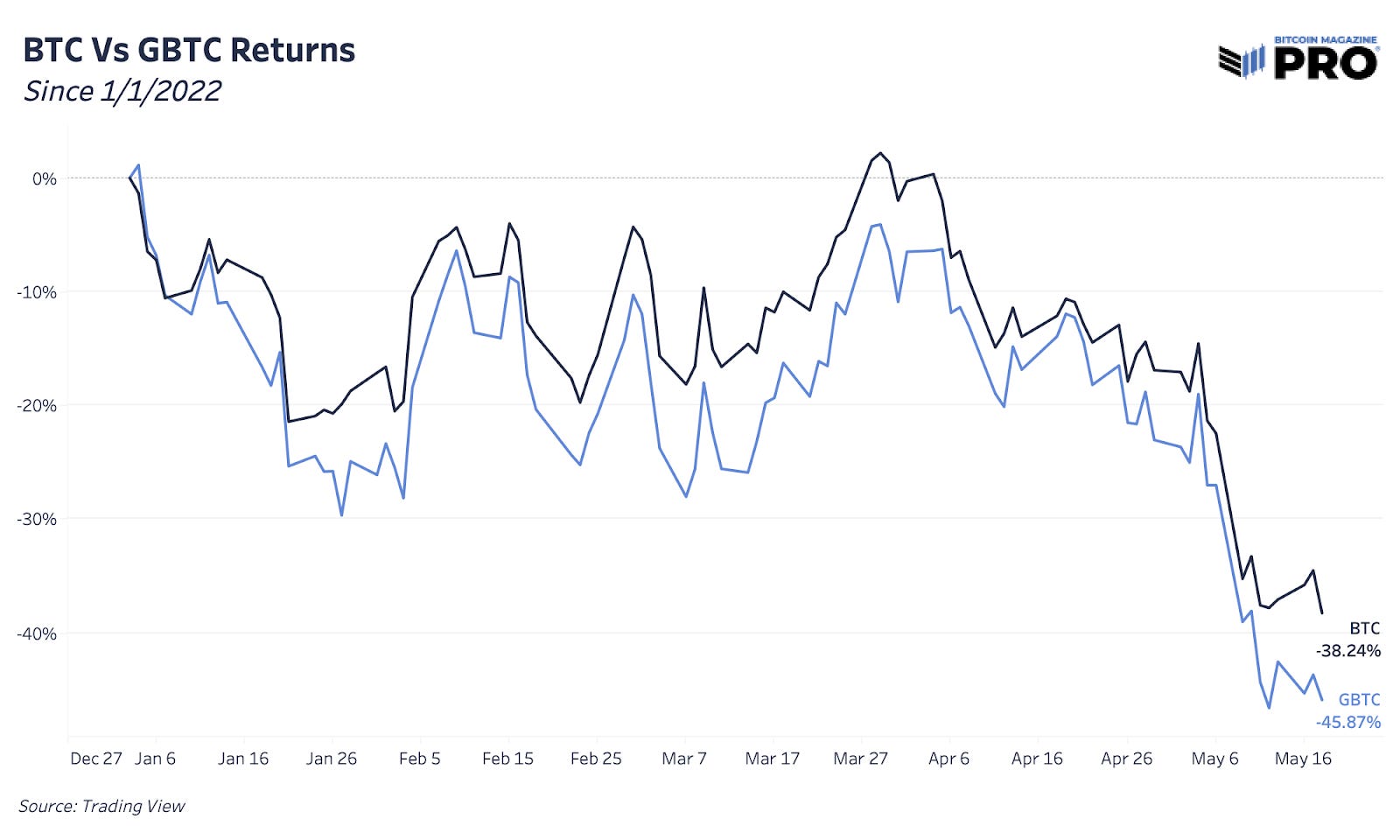

Regardless of the exact reasons for the lower GBTC discount, the lack of a bitcoin spot ETF in the United States continues to affect GBTC holders with performance down an additional 7.63% year-to-date relative to bitcoin.

With the historically steep GBTC premium flipping to a discount early in 2021, shares of GBTC are trading far below prices seen even during the 2017 bull run, burning the purchasing power of holders of the trust relative to bitcoin itself.

For funds and individuals looking to dip their toe into some bitcoin exposure, GBTC looks to be a fantastic purchase, equivalent to buying bitcoin at approximately $21,000 with a 2% annualized management fee. While it is obvious that shares of GBTC that trade in secondary markets come with none of the self-sovereign properties of the native on-chain bitcoin, if/when the trust converts to an ETF, GBTC shares offer steep upside relative to bitcoin.

The other bitcoin investment vehicle in the United States was the launch of the BITO ProShares Bitcoin Futures ETF in October 2021 which nearly marked the recent all-time high. The main concern for a futures ETF, apart from that it’s only paper-traded contracts tracking bitcoin price rather than owning bitcoin outright, has been the additional contract rollover costs and management fees. Yet in a declining market, BITO performance has tracked bitcoin performance fairly well with bitcoin outperforming by only 2.17% since the futures ETF launch date. If markets are to trade back in strong contango (futures price above the spot market price), this is when one would see the return performance widen between BITO and bitcoin.

Lastly, we have one of the most prominent bitcoin exposure vehicles over the last two years, MicroStrategy. As per their earnings presentation earlier this month, the company owns 129,218 bitcoin with an average cost basis of $30,700. As a result of their leveraged debt position to purchase bitcoin and bitcoin’s 36% year-to-date drawdown, markets are repricing the level of risk of holding MicroStrategy debt and equity. MicroStrategy is down 61.82% year-to-date while MicroStrategy’s value of bitcoin holdings now makes up 154% of their entire market cap.

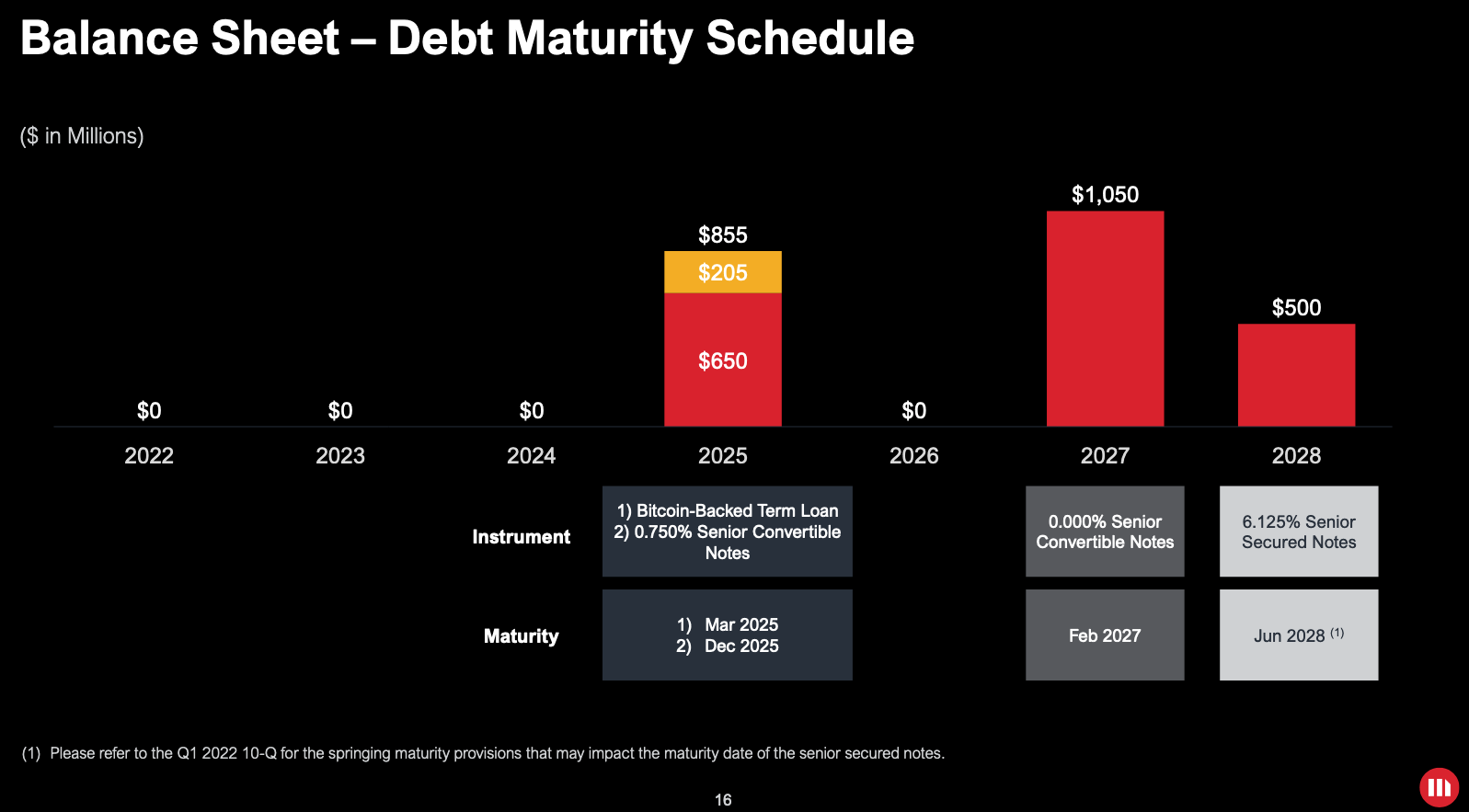

In total, MicroStrategy has taken on $2.4 billion in various debt instruments to acquire more bitcoin. With the earliest debt maturity in 2025 and the majority in 2027, Michael Saylor has taken a big bet on rising bitcoin adoption and the impacts of the network going through another halving cycle in 2024. The name of the game until then is to have adequate revenue and earnings from their software intelligence business to afford $43.7 million in annual interest expenses. Misses on both earnings and revenue in Q1 has sparked more concern for investors.

The most recent $205 million debt deal with Silvergate Bank pledges 19,466 of their bitcoin at an initial 25% loan-to-value ratio. MicroStrategy currently holds 95,643 unencumbered bitcoin that can be used at any time to top up collateral if needed.

While buying MSTR today does imply strong future expected performance in the price of bitcoin, if one is right with that assumption, shares of MSTR would be one of the best bets to make over the medium/long term, given the company’s near un-liquidatable leverage bitcoin position, and access to public capital markets along with free cash flow and a growing public brand.