Bitcoin Magazine PRO Monthly Report, May 2022 Preview

Become a premium subscriber to Bitcoin Magazine PRO to get access to this monthly report and all of the Bitcoin Magazine PRO research. We will release the full monthly report to free subscribers next Wednesday, June 8.

Sign up with the button below to get 25% off a premium subscription and access to the full report.

PREPARED BY:

Dylan LeClair, Head of Market Research

Sam Rule, Lead Analyst

Summary:

Crypto Implosion

LUNA/UST Collapse

Crypto Market Cap Destruction

Capitulation Volume Spike

Derivatives Overview

On-Chain Analysis

Mayer Multiple, Reserve Risk

MVRV Z-Score, Realized Price

HODLer Cost Basis Analysis

Macro Landscape

Macro Correlations Holding Steady

CPI Inflation, Fed Policy

Forward Economic Trajectory

Monetary Tightening Endgame

Bitcoin Mining

Hash Rate, Difficulty

Hash price, Miner Revenue

Puell Multiple, Miner Profitability

Executive Summary

We take a three-pronged approach to market analysis at Bitcoin Magazine Pro. For those who are already familiar with our process and product, all analysis is approached from the view that bitcoin is fundamentally the best monetary asset the world has ever seen. From there, we use the transparency of the Bitcoin UTXO set, the ever-changing derivatives market, and the increasingly volatile macro backdrop to help readers evaluate and contextualize the current state of the bitcoin market.

Throughout 2022, much of our focus and analysis has been around the global macro environment which has seen the highest consumer price inflation readings in four decades, leading to a deteriorating liquidity backdrop and the worst-ever year-to-date performance of the 60/40 equity/bond portfolio weighting. With the deteriorating liquidity environment, bitcoin has also fallen, often trading near 1:1 with the Nasdaq 100 tech index.

Along with the blowup of a major cryptocurrency and algorithmic stablecoin, this correlation led to a quasi-capitulation event for “crypto natives.”

In this report we will use a wide variety of data to articulate our view that bitcoin is objectively extremely cheap at current levels, along with reiterating our core thesis that it is the asset to own near the conclusion of the long-term debt cycle.

Crypto Implosion

While the macro correlations have been the dominant narrative year-to-date, in the bitcoin/broader crypto market every so often there are events that in hindsight are viewed as obvious market tops or bottoms. While it would be wrong to say that absolutely anything in this space is for certain, the LUNA/UST post mortem, and the second-order effects of its collapse, certainly look like one of those obvious moments in hindsight.

The most striking data point we see is the amount of coins that traded hands during the crash, with perpetual swap trading volume across exchanges touching levels only seen during the March 2020 and May 2021 market crashes. Similarly, spot trading volume on Coinbase (the dominant U.S. spot exchange by volume) hit levels only seen three times in history.

With the LUNA/UST crash and the subsequent liquidation of assets by many funds, the overall crypto market cap fell by as much as $570 billion dollars in a span of just six days, from May 7 to May 12.

While there are certainly flaws with measuring the value of the total cryptocurrency market by simply adding up the sum of all tokens and multiply by their circulating supply (because of the illiquidity of many alt tokens), the purpose of stating this figure is to highlight the vast amount of paper (rather: digital) wealth destruction that occurred following the LUNA debacle.

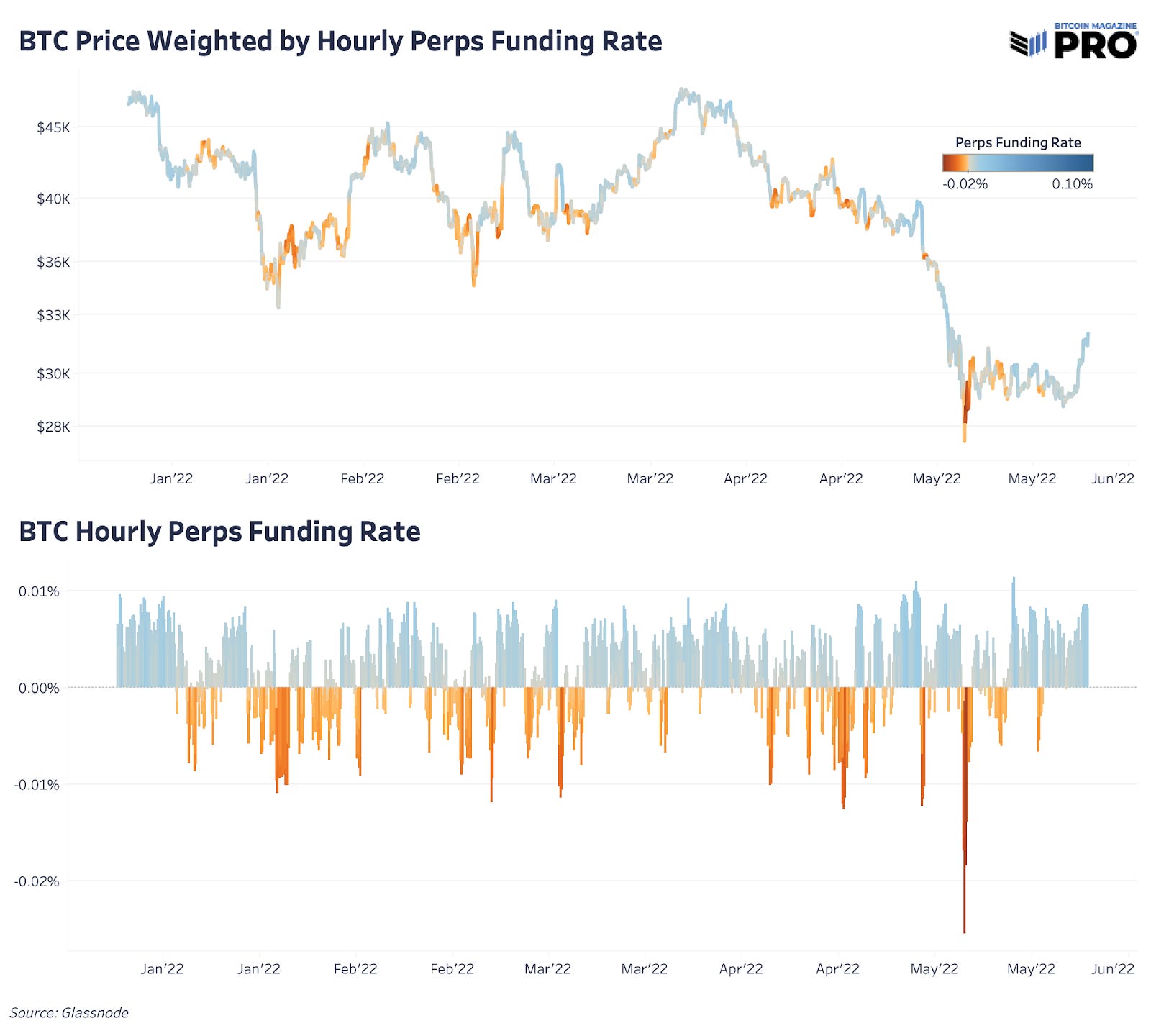

If the May low was a local or even an absolute bottom, it was different from those of the past, with a majority of selling pressure coming from spot markets rather than forced selling in the form of margin calls/derivative market liquidations.

While funding rates did go negative (price of perpetual swap contracts were below that of spot markets), it wasn’t as severe as previous market bottom events.

One of the primary reasons for why this selloff in particular wasn’t as explosive as previous liquidation events was the structural change in the bitcoin derivatives market that has been underway for the last year. The collateral underlying derivative contracts has shifted from 70% bitcoin margined, to just 40% with the other 60% being collateralized with stablecoins such as USDT.

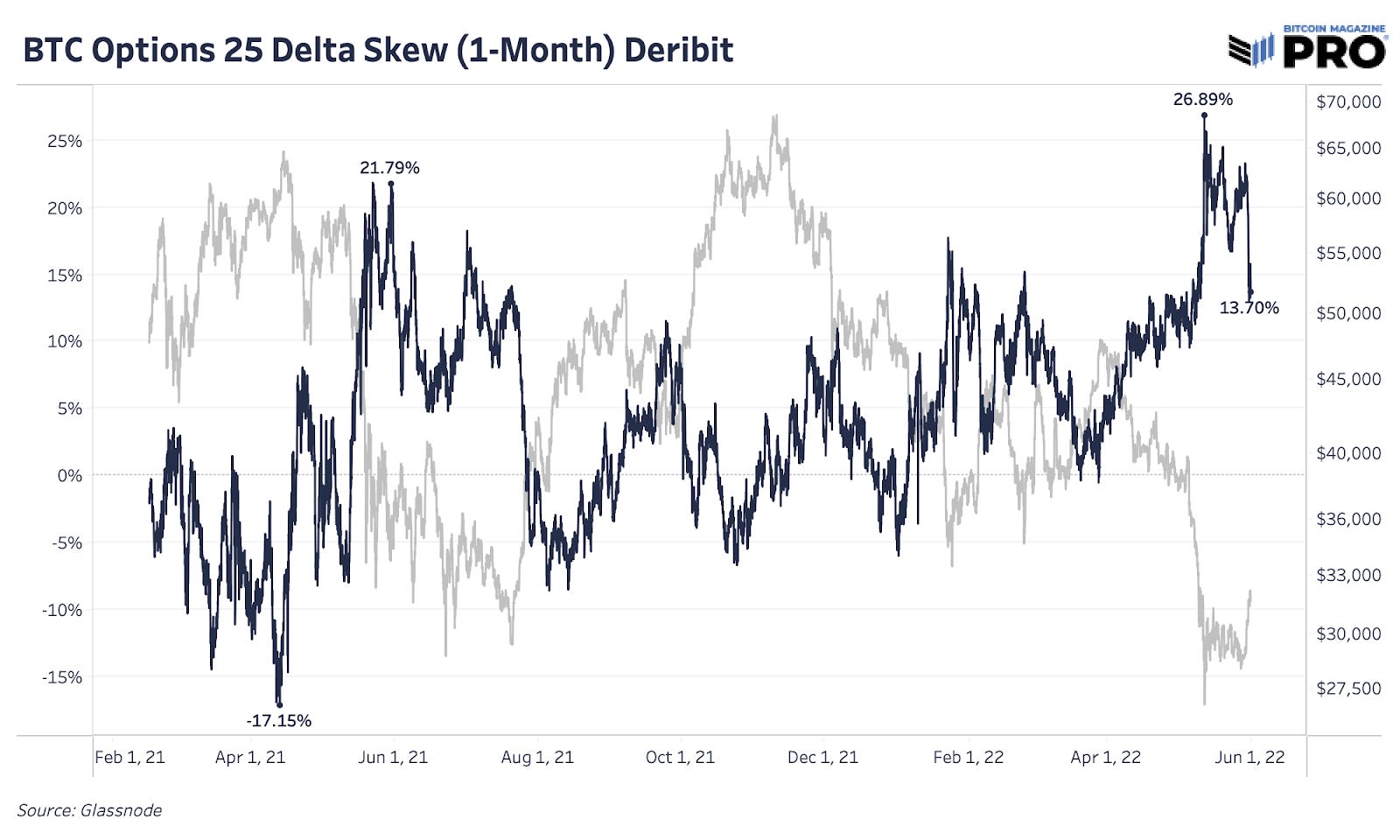

Lastly, while the options market is a bit more esoteric, we can observe the 25-delta skew, which in layman’s terms measures the relative premium placed on put and call options. When the figure is positive, it shows that options traders are willing to pay more for downside protection in the form of puts; when the delta skew is negative, it shows that calls are more expensive (higher implied volatility).

While it’s not our intent to go fully into the weeds on the dynamics of the options market, the main takeaway is to highlight the feverish demand for downside protection during market sell-offs, while also displaying the demand that call options garner during speculative frenzies at market tops. Thus, the relative richness of put options during the market sell-off was quite notable, as it’s the highest reading seen in the history of the data.

One of the best strategies in any market, but specifically in the still nascent bitcoin market, is to back up the truck to buy when others become forced sellers. This often comes in the form of liquidations in the derivatives market, with spectacular unwinds coming sporadically once or twice a year. While this specific market event wasn’t the usual derivative market liquidation event, there was the forced liquidation of the Luna Foundation Guard’s multi-billion dollar bitcoin stash, along with the sell pressure that came from other crypto funds.

Market Cycle Dynamics On-Chain

Our cyclical indicators use both price as well as on-chain dynamics to gauge bitcoin’s relative valuation compared to historical standards. With there being plenty of variables to account for, we find that many of the cyclical indicators do a great job of stripping back all of the noise, sentiment and narratives to objectively display whether bitcoin is relatively cheap or relatively expensive.

The Mayer Multiple, coined by Trace Mayer, simply evaluates the bitcoin price relative to its 200-day moving average. Historically, any reading below 0.8 has served as a tremendous buying opportunity. The current Mayer Multiple reading is in the ninth percentile of historical readings.

The RHODL Ratio takes the ratio between the realized market capitalization of bitcoin, one-week and 1-2 years old. In simple terms, it evaluates how top-heavy the market is using the transparency of the bitcoin blockchain.